Presenting the Fed’s Perfect Plan for U.S. Dollar Oblivion

The Federal Reserve adjourned its annual meeting in Jackson Hole, Wyoming on August 26, 2023 without fanfare but not without consequence.

As always, lots of papers were presented by established figures in the art of monetary tinkering and manipulation at this year’s Jackson Hole meeting. Most papers amount to esoteric confetti, as rewarding as garden variety TikTok videos only utterly denuded of thrill. Occasionally, however, a paper turns out to be a blueprint for a tectonic shift by the Fed. That appears to be the case this year, which is the subject of this video.

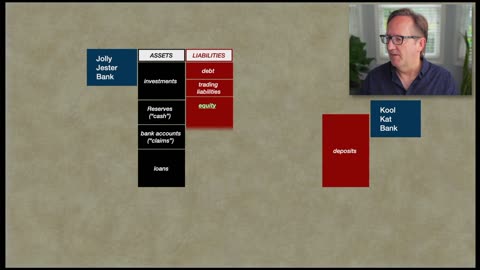

As a reminder to viewers, the last time a Jackson Hole paper gave rise to a major monetary shift was in 2019, when BlackRock presented a paper entitled, “Dealing with the Next Downturn.” As luck would have it, the title downturn arrived with the repo crisis of September 2019 followed up by the rollout of Pandemic!!! six months later. Crucially the Fed’s response to those events—creating $5T in new reserves PLUS $5T in new bank deposits, in accordance with BlackRock’s paper—represented a material departure by the Fed from its response to the GFC in 2009; back then, the Fed was acting to bail out the banks, which it did by creating, say, $2T in new reserves without any need at all for new bank deposits.

To summarize: • 2009—no new deposits created by Fed, no inflation. • 2020—Fed creates $5T of new bank deposits, gets big time inflation. • HUGE difference.

This channel produced a video about BlackRock’s 2019 paper entitled, “Larry and Carstens’ Excellent Pandemic.”

Flash forward to the recently-adjourned 2023 Jackson Hole meeting. There is one particular paper that, if implemented, would cause huge inflation and indeed piggyback on and turbo-charge the inflation that’s arisen from the Fed’s implementation of BlackRock’s 2019 paper.

You can find a more complete description of the current video here: https://bestevidence.substack.com/p/presenting-the-feds-perfect-plan

You can find links to materials covered by the video, including the 2023 Jax Hole paper and Marriner Eccles’ March 1947 congressional testimony explaining what will happen if the Fed implements that paper, in the substack link above.

-JT

2.36K

views

24

comments

Deep Diving the Fed's Killer Whale Crisis

00:00 Intro - the “regional banking crisis” label is deceptive and laughable

02:13 Solvency vs. liquidity

04:55 Visual depiction of a liquidity crisis

10:30 1st way bank liquidity (deposits) is created: bank loans

11:51 2nd way bank liquidity (deposits) is created: Fed asset purchases from non-banks

16:17 This crisis—a liquidity crisis—is caused by the Fed’s creation of whale deposits

17:15 Senate hearing confirms: whale deposits killed Silicon Valley Bank

20:46 Killer whale deposits, not apps, caused this banking crisis

23:05 Forensic evidence proves Fed created whale deposits

27:39 Shills who say the Fed can’t create bank deposits are lying

29:40 How the Fed passed trillions of dollars to the whales

32:51 The Fed passed money to legal entities, which in turn passed it to whales

37:35 Pandemic QE was designed to produce whale accounts

39:43 The Fed lied when it said Pandemic QE was for “price stability”

41:45 Why were whale accounts maintained for years if not to become killers?

43:00 Whale accounts are maintained by criminals

46:13 Red Flag Test #1 for banks

53:07 Presenting the BestEvidence spreadsheet of $100 billion banks

55:53 Red Flag Test #2 for banks

1:03:35 This crisis is nudging the U.S. closer to CBDC

1:06:06 The names of the Fed’s killer whales are a big secret—for now

1:07:15 Congress could get to bottom of this crisis in 30 days if it wanted to

1:09:13 How you can help BestEvidence

This video was originally gonna be called, “The 2023 banking crisis would rank as the most obvious crime scene of all time if pretty much the entire financial services industry didn’t have its head up its A$$ about Pandemic QE,” but that title didn’t test well in focus groups.

Alas, and from the top…

Having stood alone in predicting the 2023 banking crisis three weeks in advance, BestEvidence in the present video turns to the question of causes. Over the course of some 71 minutes, “Deep Diving the Fed’s Killer Whale Crisis” proves beyond any doubt that the Federal Reserve is to blame for this crisis and is very likely controlling it even now, while this so-called “regional banking crisis” (quite easily the dumbest name ever for a financial event) is in apparent remission.

It’s highly unlikely you’ll ever stumble across any of the following truths about the crisis in the Wall Street Journal or any other outlet of any significant reach.

-This is a liquidity crisis, not a solvency crisis

-The liquidity in question that is driving this crisis sits in massive bank deposits in the household sector of the economy, not in the other sectors

-when just a handful of said massive deposits leave a bank, the bank gets killed, hence the name of this video

-The Fed created those bank deposits and has admitted as much (cue the chorus of feces-throwing monkeys in the financial services industry to try and screech away the Fed’s own admission on this point)

-The Fed created those bank deposits by buying assets from non-banks, and thus congress should demand a complete list of asset purchases made by the Fed starting March 2020

-The Fed lied through its teeth when it said those assets purchases were made for purposes of “price stability”

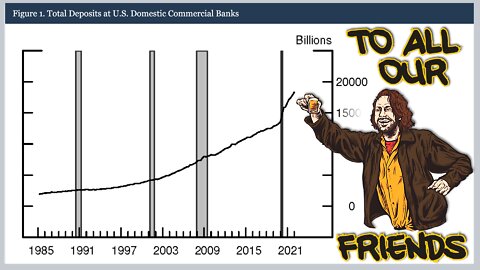

-Under the Fed’s asset purchases, the average household checking account of the top 0.1% wealthy households grew from $565,000 in 1Q2020 to $5 million in 1Q2022; this is the locus of killer whale deposits

-All three dead banks so far (Silicon Valley Bank, Signature Bank, First Republic) exhibited 2 fatal distress signals shortly before they died—both of which distress signals can be tested for with respect to banks that have not yet been taken down by killer whales

All that and so much more…

-JT

Footnotes

(01) Debt by Design: Banking Facts and Fallacies (2017), by Joshua Maree; available as pdf at https://www.fairmoney.info/wp-content/uploads/2017/08/Fair-Money.pdf

(02) "Understanding Bank Deposit Growth during the COVID-19 Pandemic," June 3, 2022, by Andrew Castro, Michele Cavallo and Rebecca Zarutskie; see https://www.federalreserve.gov/econres/notes/feds-notes/understanding-bank-deposit-growth-during-the-covid-19-pandemic-20220603.html

(03) "Fed Admits Crony Truth About Pandemic QE: 'it creates new bank deposits,'” Sept. 5, 2022, by John Titus; see https://www.youtube.com/watch?v=n1xgQeCiu6k

(04) "Senate Banking Committee hearing on the collapse of SVB and Signature Bank," March 28, 2023, at 45:26: https://youtu.be/JpyR-Q2eiIc?t=2726

(05) Checkable Deposits And Currency Held by the Top 0.1% (99.9th to 100th Wealth Percentiles); see https://fred.stlouisfed.org/series/WFRBLTP1228#0

(06) Total Households; see https://fred.stlouisfed.org/series/TTLHH

(07) Barfly (1987); see https://www.imdb.com/title/tt0092618/?ref_=fn_al_tt_1

(08) Households; Checkable Deposits and Currency; Asset, Level; see https://fred.stlouisfed.org/series/BOGZ1FL193020005Q

(09) "Federal Reserve Actions to Support the Flow of Credit to Households and Businesses," Mar. 15, 2020; see https://www.federalreserve.gov/newsevents/pressreleases/monetary20200315b.htm; see also "Federal Reserve issues FOMC statement," Mar. 15, 2020 ("...to foster maximum employment and price stability...." the FOMC "will increase its holdings of Treasury securities by at least $500 billion and its holdings of agency mortgage-backed securities by at least $200 billion."); see https://www.federalreserve.gov/newsevents/pressreleases/monetary20200315a.htm

(10) JPMadoff: The Unholy Alliance between America's Biggest Bank and America's Biggest Crook (2015), by Helen Davis Chaitman and Lance Gotthoffer.

(11) U.S. Money vs. Corporation Currency: "Aldrich Plan," Wall Street Confessions!, Great Bank Combine (1912), by Alfred Owen Crozier.

(12) https://banks.data.fdic.gov/bankfind-suite/financialreporting (RED FLAG TEST NO. 1)

(13) https://bestevidence.substack.com/

(14) https://cdr.ffiec.gov/public/ManageFacsimiles.aspx (RED FLAG TEST NO. 2)

(15) To help BestEvidence per 1:09:35, or just to send a hello postcard…

John Titus

9660 Falls of the Neuse Rd.

Suite 138, No. 241

Raleigh, NC 27615

1.54K

views

21

comments

Why Is the Federal Reserve Provoking a Financial Crisis?

Timestamps

1:23 - Global risk posed by U.S. banking system

2:30 - Repo crisis preceded PANDEMIC!!!

3:32 - WEF’s tote board of risk narratives

4:05 - F.D.I.C. Quarterly Banking Profile (3Q2022): real risk of banking crisis

5:26 - Chart 7 of Quarterly Banking Profile - massive balance sheet losses

8:41 - Why debt-based securities dropped in value by $690 billion

11:40 - Composite balance sheet (entire industry) in Quarterly Banking Profile

14:33 - Why assets on banks’ balance sheet are vastly over-valued

17:12 - That entire banking industry is dead broke, evident from composite liabilities

20:10 - Banks’ counter-measures to their insolvency

21:32 - FHLB advances: panic borrowing

24:57 - Repo market: more panic borrowing

26:54 - FRED’s tale of three crises

35:23 - Role of FHLB advances in last three crises

39:52 - Panic borrowing now - Fed fanning flames of new crisis

41:25 - New era has dawned: Snake Eating Its Own Tail

This video builds on and extends the explosive (but largely overlooked AFAIK) analysis done by Chris Whalen, “Is JPMorgan Chase Insolvent?” While Whalen is imo the best independent bank analyst in the business, he doesn’t have a crystal ball. (At least I couldn’t find one when I ransacked his home many moons ago.) He put out that post, which is nominally about Dimon’s bank but covers the entire banking industry, on Monday, November 28, 2022. He thus didn’t have access to the F.D.I.C.’s Quarterly Banking Profile for the 3rd quarter of 2022, which came out three days later. Whalen’s analysis focused on the dubious valuations of bank assets, which is certainly germane as far as they go and are discussed in greater detail in this video.

The real action in the third quarter QBP, though, is on the liability side of the industry’s balance sheet. There we find evidence that aside from being broke, the banks know they’re broke and are panicking about it.

But here’s the real kicker: the Fed isn’t helping the banks this go-round. It’s a new ballgame, and it goes by the name ALL. BAD.

You can find more detailed written treatments of this video and others I’ve done at my substack: https://bestevidence.substack.com/

* * * * *

Links

Chris Whalen’s November 2022 (in)solvency assessment of banking industry:

https://www.theinstitutionalriskanalyst.com/post/is-jpmorgan-chase-insolvent

World Economic Forum’s 98-page global risk assessment (2023 edition):

https://www3.weforum.org/docs/WEF_Global_Risks_Report_2023.pdf

F.D.I.C. Quarterly Banking Profile:

https://www.fdic.gov/analysis/quarterly-banking-profile/index.html

Basel III regulations - Definition of capital excludes goodwill:

https://www.bis.org/basel_framework/chapter/CAP/30.htm

New York Fed’s take on Federal Home Loan Board (FHLB) during GFC:

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr357.pdf

Uncle FREDdie:

https://fred.stlouisfed.org/

Mish Shedlock’s post on exploding interest payments on U.S. debt (Feb. 5, 2023):

https://mishtalk.com/economics/the-annual-interest-rate-payment-on-government-debt-is-850-billion-and-rising-fast

934

views

25

comments

Fed Admits Crony Truth About Pandemic QE: “it creates new bank deposits”

Ahhhh, so it turns out that the Federal Reserve CAN shovel money directly into retail bank accounts, and did so for two full years under cover of PANDEMIC!!!

BestEvidence has stood alone in making exactly that point repeatedly over the last two years, defying the financial pundits who sought to quell any concerns about what exactly the Fed was doing with solemn assurances that, no, you silly serf with your pesky concerns—the Fed’s QE programs have no effect whatsoever on the retail money supply because [insert Fed-apologizing snake oil here] “reserves don’t leak out into the banking system.”

BestEvidence is pleased to announce that in its quixotic quest to bring light to the shameful QE darkness cast by said pundits, the channel has picked up a new ally: the Federal Reserve itself. Well, a team of Fed researchers, anyway.

For those keeping score at home, it’s now official:

BestEvidence 3

Financial Gurus 0

Far more interesting, though, than a bunch of hoity-toity financial pundits having their face masks adorned with a thick layer of egg, is what the Fed’s admission about Pandemic QE reveals about the privately owned central bank’s actions over the last 12 years. As always, follow the money…

https://bestevidence.substack.com/p/fed-admits-crony-truth-about-pandemic

523

views

21

comments

Two Weeks to Flatten Your Country

Presentation given by BestEvidence’s John Titus at Doctors for Covid Ethics’ fourth symposium, dated June 11, 2022.

https://bestevidence.substack.com/p/two-weeks-to-flatten-your-country?sd=pf

This presentation appears at 4:36:22 of original Rumble post:

https://rumble.com/v180hjf-doctors-for-covid-ethics-fourth-symposium-freedom-is-the-cure.html

The video features a clip from that unparalleled masterpiece of activist journalism, Martin Smith's "The Untouchables" episode of PBS Frontline. You can see it here: https://www.pbs.org/wgbh/frontline/documentary/untouchables/

2.29K

views

43

comments