Why are annuities considered bad investments?

Why are annuities considered bad investments?

Annuities provide a guaranteed income during retirement. Despite the benefits they offer, they are overall a poor investment choice for several reasons that we will explore today. Finally, I will offer alternatives to annuities, and the best approach to doing an annuity if that is really the best choice or the preferable choice for you and your financial situation. If you are not staying for the entire video, let me warn you the high commissions sales people earn on annuity products. Do not allow a salesperson to do what is in their best interest, earning a high commissions, by selling you a financial product that may not make any sense for your financial situation.

They are intended to alleviate the fear of a retiree outliving their assets. After all, people are living longer, and many people will outlive their savings. Many of us will unfortunately find that our assets are not adequate to maintain our standard of living throughout our retirement. Therefore, annuities are particularly attractive for people that believe they will have long lives and risk outliving their assets. Therefore, annuities are a way to hedge against longevity risk, that is, the longevity of your own life.

They provide a steady stream of income over a specified period of time or the lifetime of the person who purchased the annuity. They can supplement retirement income by creating predictable cash flow. They are considered a type of insurance contract.

The first stage of the annuity is called the accumulation phase. The investor would purchase an annuity with either a lump sum or monthly premiums. Payments would commence during the annuitization period and continue either for a fixed period or for the rest of the life of the annuitant.

There are two types of annuities: immediate or deferred. Immediate annuities are purchased by people of any age that want to exchange a lump sum of money for cash flows in the future. So an immediate annuities is when we are immediately trading a lump sum of cash for future cash flows. A deferred annuity refers to a delay in when you will receive the cash payments. The money you are paying either as a lump sum or as monthly premiums is going to be invested by the company you purchased the annuity from.

Annuities can be either fixed or variable. A fixed annuity is going to pay a specific rate of return on what you invested. In contrast, a variable annuity is going to invest the money, and the returns will fluctuate.

The con that most people focus on when it comes to annuities is the high commissions. A financial advisor stands to make 6% to 8% or more in commission from selling an annuity versus 2% for a mutual fund. When we are talking about rolling over $500,000, the advisor stands to make $10,000 for the mutual fund versus $25,000 to $35,000 for the annuity. Therefore, it is in the financial advisors best interest to direct as many clients as possible into annuities because the commission is two or three times or more than that for a mutual fund.

Annuities have high fees that are not apparent at first. There are annual maintenance and operational charges that are considerably higher than that for mutual funds. There has been a lot of public backlash against these exorbitant fees and many insurers are having to reduce the expenses. However, low expenses are not a given and it is something that should be reviewed before you commit to a financial product.

Once money is tied up in an annuity, it is made purposely difficult to retrieve it. There are hefty surrender fees charged by the insurer to get the money out of an annuity before a period time has elapsed which is usually six to eight years, but sometimes even longer. There are also tax penalties of ~10% for early withdrawal.

Annuities already are tax sheltered. Therefore, it is redundant and offers no additional benefit to put an annuity in an IRA despite the urging of overly eager salespeople.

Annuities should only be considered by those with straightforward finances that desires simple and fixed payments. Annuities are not necessary for everyone despite being one of the most established way to save money for retirement. It is critical to evaluate all the possible fees associated with any financial or insurance product you are considering.

Alternatives to annuities include deferred compensation plans like 401(k)s, IRA, dividend paying stocks, variable life insurance, and retirement income funds.

Works Cited:

https://www.investopedia.com/articles/retirement/08/annuity-mutualfund.asp

https://www.investopedia.com/terms/a/annuity.asp

Tags:

annuities, what are annuities, annuities explained, are annuities bad, are annuities a good investment, are annuities good investments, why are annuities bad, why annuities are bad investments, annuities are bad investments, are annuities investments, types of annuities, annuities for retirement, pros and cons of annuities, are fixed index annuities a good investment, annuities in retirement, retirement annuities, annuities for dummies, why variable annuities are bad

92

views

Why are businesses increasingly relying on tips to compensate their workers?

Why are businesses increasingly relying on tips to compensate their workers?

During the pandemic, customers tipped workers to acknowledge the risk they were exposing themselves to. Businesses have become reliant on the practice of tipping for an increasing share of employee compensation as most employers have tight margins.

Despite current news and economic data, many people, including myself, believe there could be an economic recession. Many businesses also expect economic turmoil in the near future which is why they are reluctant to lock in higher employee wages. Tipping pushes the financial risk onto the workers rather than the employer.

There are few sectors where it is so hard to hold onto workers than the service sector.

The quit rate for workers in lodging and food service is ~5% over three months since July 2021 versus ~3.3 in retail, and the overall quit rate of ~2.6 accord to the Bureau of Labor Statistics.

Tipping increases worker compensation which makes it easier to retain workers.

Tips as a share of compensation are rising faster in limited service establishments like bakeries and coffee shops rather than full service places like restaurants. I think this is because we were not tipping at these limited service establishments in the past, whereas it has always been customary to tip at a sit down restaurant.

A business has a duty to charge a fair price in the market. If a customer feels the price is too high, they will not return to the business. It makes me think of a new place I stopped for lunch on the way home that I will not return to because I felt the price was too high.

Tips potentially motivate employees, giving them an incentive to work harder or better.

Being prompted for a tip is probably more awkward for the customer than it is for the worker.

Most businesses fluctuate seasonally which means tipping rises and falls. Many service workers are lower income and struggle to deal with volatility in pay.

Increasing reliance on tips to compensate workers, without increasing base pay, is arguably detrimental to workers in the long term. At any time, there would be a reduction in tips that effectively lowers a worker’s overall pay. In fact, customers are tipping less often than they were at the height of the pandemic. As a society, we are reaching an inflection point where we are starting to acknowledge that tipping culture has gotten out of hand.

Works Cited:

https://www.wsj.com/articles/tipping-businesses-cant-stop-asking-cc1aca6c?mod=hp_lead_pos7

Tags:

tipping culture, tipping, tipping culture in america, tipping culture in usa, tipping culture out of control, the tipping culture in america is broken, tipping culture in america is out of control, tipping culture in america history, tipping culture is bad, tipping culture debate, tipping culture is toxic, america tipping culture, american tipping culture, american tipping, tipping in america, culture, tipping point, tipping in the usa, history of tipping

51

views

Why are crypto stocks outperforming bitcoin?

Why are crypto stocks outperforming bitcoin?

While bitcoin has rallied about 80% this year, that pales in comparison to Coinbase, up 190%, MicroStrategy, up 210%, and Grayscale Bitcoin Trust, up 140%.

We are still below record highs for all these assets.

So why did all of these have such larger rallies than bitcoin? Well, for one, they are more volatile. Another reason, they were potentially more oversold than bitcoin was. However, I will argue that largest reason is institutional and retail investor adoption.

A lot of people are not very savy with technology. With Coinbase, Microstrategy, and Grayscale Bitcoin Trust, you can just log onto your brokerage account and purchase them. It’s that easy. With a cold wallet, you have to worry about a physical device, and its seed phrase. Is the seed phrase safe? Where is your seed phase? With the three stocks I mentioned, they can just sit in your brokerage account online?

If you are wondering how much your stocks are worth, you can just log onto your account and check it out? Want to add to your position, or sell some shares for cash? It’s a piece of cake. You can do it from the bathroom, or on your jog.

Tags:

coinbase, coinbase lawsuit, coinbase sec, coinbase news, sec coinbase, coinbase ceo, coinbase vs sec, sec vs coinbase, coinbase wells notice, coinbase app, coinbase stock, coinbase crypto, coinbase handel, coinbase sues sec, coinbase trading, coinbase analyse, sec sues coinbase, how to use coinbase, coinbase sec lawsuit, coinbaser, use coinbase, coinbase etf, coinbase usa, coinbase v sec, cboe coinbase, coinbase sued, coinbase vs sev, how to coinbase

23

views

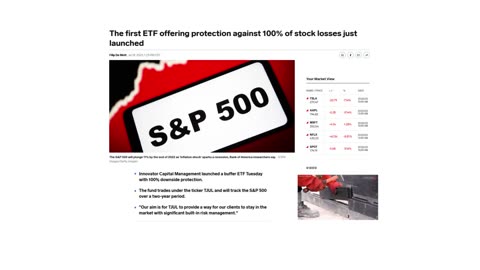

What is a “protection” ETF?

What is a “protection” ETF?

A protected ETF is an investment in the stock market with a protective collar strategy. It is essentially a structured project where most of the money is invested in the stock market, and then a small amount of money is invested in a put at the current strike price. It is a long ETF with a collar (long put, short call).

By investing in the stock market, the ETF is long the underlying asset. To protect against large losses, the ETF will purchase an out of the money put option to protect the investor. A put option is the right, but not the obligation, to sell at a specific price. So the ETF is securing a price to sell at, this costs money, but offers protection. They will also write an out of the money call option to produce some income, ideally to offset the cost of the put. A call option is the right to purchase an asset at a price. The ETF is selling the right for a buyer to purchase something. So essentially, the ETF secures a selling price to protect investors, which costs money, they generate some money by selling the right for a buyer to purchase the equities at a certain price.

Protection ETFs are also known as buffer ETFS or defined outcome funds. They are an alternative to insurance products like fixed-income annuities.

The Innovator Equity Defined Protection ETF, ticker: TJUL, the first exchange traded fund aiming to provide 100% downside protection, launched in July of 2023. It has a relatively high expense ratio of 0.79%. It is important to note that if the ETF increases in value after launch, any gains will not be protected.

Big upsides help the long term averages much more substantially than people think. The ~10% return the S&P averages is the average of low and high annual returns. You need ~20% bull runs to offset years where the annual return may be negative.

This product may be attractive to people in their 60s that are about to retire.

Works Cited:

https://markets.businessinsider.com/news/etf/buffer-etf-downside-protection-innovator-tjul-stock-losses-insurance-market-2023-7

https://www.investopedia.com/terms/c/collar.asp

Tags:

buffer etfs, buffer etf, etf, s&p buffered etf, first trust buffer etf, buffer, etf edge, buffered etf, buffer etfs invest, buffered etfs, invest in buffer etfs, buffered notes, buffered mutual funds, buffer funds, buffered etfs summary, buffered etfs explained, buffered annuities, what are defined buffered, buffered exchange traded funds, vti etf, #bufferetfs, best dividend etf for long term, best dividend etf to hold forever, growth etf 2022, etfs. Active

17

views

Is now the time to exit real estate in Florida?

Is now the time to exit real estate in Florida?

There is no denying the strength and momentum of the real estate market in Florida. Some people would argue that the Florida real estate market is effectively indestructible at this point but I would counter that these circumstances could describe a bubble. Despite this, is it time to pack up, sell the house, and exit the state? There are a number of considerations to be made, and the decisions will be extremely location orientated, as well as based on personal factors like your age and wealth.

The largest issue with real estate in Florida is the insurance rate premium. Florida’s real estate market is extremely hot despite exorbitant insurance premiums.

Florida is getting to a point where real estate is uninsurable or prohibitively costly to insure. Many people in Florida do not have insurance because it is so expensive. This leaves them susceptible to a storm wiping out all the value in their home. Home insurance is something you really should not live without. A standard policy covers the replacement of the home and some of its contents in the even of damage or theft. If you lose your house, and it isn’t insured, you will probably lose all the contents of the house as well.

If you think insurance costs are bad now, future storms could drive the rates up further. Even areas that are several miles inland are still risky bets when it comes to hurricanes and storm damage. Homeowners will likely experience more storm damages and additional issues before there is any chance insurance rates decrease. High property insurance costs will hamper or decrease property values in a similar way that high taxes do.

Home prices in other parts of the country like the Northeast, Northwest, and West are much higher than Florida. The price of a house in Tampa is about half the price of cities like Boston, New York, DC, Seattle, Portland, San Francisco, and LA. In addition, other parts of the country have far higher property taxes for a comparable house. Given this, it could potentially make sense to purchase property in Florida, or stay in Florida, if you are far enough away from the water.

The need to flee California and New York due to covid is largely over which has lessened upward price momentum in Florida real estate.

The Florida insurance crisis may just be beginning. It may be a fools errand to try and wait for insurance costs or mortgage rates to decrease. Insurers are financially stress as they case losses from severe weather, inflation, and supply chain bottlenecks. This leads them to jack up rates. The issue is more than just bad weather, there is also runaway lawsuit abuse in Florida.

In the past few years in Florida, seven insurers have gone belly up, 15 have stopped writing new business, and four have abandoned the state entirely. If insurers are fleeing Florida, should you?

Works Cited:

https://www.reddit.com/r/RealEstate/comments/153gfwc/giving_up_on_florida_real_estate/

Tags:

florida real estate, florida real estate market, florida real estate market analysis, real estate market update, tampa florida real estate, tampa real estate, real estate 2023, moving to florida, real estate florida, homeowners insurance, homeowners insurance florida, florida insurance, property insurance, homeowners insurance coverage, florida, florida homeowners insurance, home insurance florida, homeowners insurance policies, insurance, home insurance, homeowners insurance claims, homeowners insurance premium, florida homeowners insurance issue, florida homeowners insurance crisis, best homeowners insurance companies in florida, florida homeowners insurance crisis getting worse

151

views

Why is southern Italy so much poorer than northern Italy, and why it will remain that way.

Why is southern Italy so much poorer than northern Italy, and why it will remain that way.

The poverty that exists in southern Italy is in stark contrast to the wealth on display in the north. Most tourists never make it much farther south than Rome. If they did, they would be surprised at how rural and impoverished southern Italy is. The persistent economic disparity between Southern and Northern Italy is due to a number of factors that we will explore. I believe this stark disparity in wealth will continue for the foreseeable future.

It's worth noting that Italy is relatively wealthy country, and the poverty of the south is relative, when all things are considered. Sicily, Italy’s poorest province, has a similar Human Development Index score to Slovakia, Hungary, and Puerto Rico.

Geographical Factors:

Let’s consider the topography of Italy. To the north of Italy you have the Alps, the highest and most extensive mountain range in Europe. Most of Italy’s water comes from the Alps. From the western Alps flows the Po river to the Adriatic Sea. The Po River has one of the longest contiguous flows surrounded by flat, fertile land in Europe. 17 million people, or about a third of the total population of Italy, live in this area. The rich fertile farmland of the Po valley contributed to north being wealthier. Richer areas of Italy overlap with the Po river. Perhaps, just as important as fertile land, is the transport afforded by a large river. The Po River gave the valley access to both Genoa and Venice which were major port cities since the Middle Ages, facilitating trade with the east.

It cannot be overstated the impact naval trade had on northern Italy as it was a significant driver of economic activity in the late Middle Ages and renaissance. Venice and Genoa exerted considerable control over Mediterranean trade. They possessed exclusive rights to Constantinople and the Black Sea. They were employed by crusading armies to ferry troops to the middle east.

Historically, the Kingdom of Naples dominated the south in contrast to the north which was organized into various mercantile city states that competed against one another. The cities of Rome, Florence, Milan, and Genoa are all in the North. The south only has Naples. Typically, Italians divide their country in north, central, and south. In which case, Rome and Florence may be considered central Italy. However, for our purposes, we will divide the country into north and south.

The south does have some fertile areas, but more importantly, it has several good ports which are conducive to trade. The cities of Naples, Palermo, Catani, and Bari all have a combination of good ports and fertile land which would lend itself to be a fairly well off and populated region or city.

Due to the heat and oppressiveness of the midday sun, southern Italy, as well as most areas with a similar climate and geography, tend to take off during the time the sun is hottest, returning to work in the evening. In contrast, northern European work cultures tended to work a continuous period from morning to early evening.

Historical Context:

Italy was unified under the Roman Republic in the third century BC, and remained realtivley whole even after the fall of the Roman Empire under the Ostrogoths until it became disputed between the Kingdom of the Lombards and the Byzantine (Eastern Roman) Empire.

Italy was a divided nation from Justinian in the 500s to Napoleon in 1798. The north largely existed as small independent city-states, while the south was ruled as a territory of a distant emperor.

The first Holy Roman Emperor, Charlemagne, conquered northern Italy, as far south as Rome, but his southern campaign failed to make lasting gains. The Holy Roman Empire continued to rule Northern Italy for hundreds of years while not making permanent gains in the south which was held by the Byzantine empire, and occasionally Islamic forces.

Southern Italy was subjected to destruction and devastation repeatedly as warring empires and nations fought over it

Historically, the cities of Genoa, Venice, and Florence were economic power houses during the late medieval and renaissance period. Wealth accumulated and spread across the regions closest to these cities. When the industrial revolution arrived in Italy, investment in workshops and factories occurred primarily where that wealth was found: northern Italy. It is worth mentioning that the lack of a unified Italy was a factor in preventing the spread of wealth and investment in the south. However, I would argue even if Italy was unified before the industrial revolution, the wealth and investment still would have heavily concentrated in the north, and this great north-south disparity would still have persisted.

Eventually, northern Italy was overshadowed by Spain, the Netherlands, and Britian due to their grip on global trade. Italy lagged the rest of the developed world, and was in a state of turbulence and upheaval, until its reunification in 1871.

The importance of finance in modern civilization cannot be understated

Reunification:

I would be remiss if I did not acknowledge that Italian reunification caused widespread destruction of southern Italy in contrast to the north that was largely left intact.

Italian unification was conducted primarily by the northern state of Sardinia-Piedmont with its capital in Turin. This kingdom was composed of what is now southeastern France. It was more aligned with northern Europe than the Mediterranean. The money and investment would naturally flow around the capital. Southern Italy was not keen on reunification, especially by another state. They desired to be in control of the process if it was going to occur. Arguably, the south was punished in a way by receiving little investment.

It is worth considering the economic disparities between what was formerly eastern Germany versus western Germany. Germany arguably handled the merging of the country better than Italy, and yet dramatic disparities still persist.

The south is more agrarian because it was run as a feudal state

Industrialization:

The industrial revolution began in Britian and flowed out of London to aligned nations and areas that had close cultural and economic ties.

Northern Italy is relatively industrialized. In fact, industry was the only path to some level of prosperity given Italy’s lack of natural resources and fertile land with the exception of the Po Vallye.

In contrast to the north’s industrial orientation, the south has primarily been an agricultural economy.

Silk production was an important economic driver of northern Italy in the early twentieth century.

Emigration and Brain Drain:

Arguably, a country’s greatest resource is its people. The drain of human capital out of southern Italy to the Europe and the Americas significantly hindered development of southern Italy.

Southern Italians have immigrated to both northern Italy, and the rest of the world, for hundreds of years in search of opportunities and a better life. Perhaps this is why southern Italian cuisine is so globally widespread. Consider the prevalence of tomatoes in Italian American cooking.

Discrimination:

Southern Italians faced discrimination in the United States partly due to their darker skin tones and adherence to Catholicism. Northern European Protestants were more quickly assimilated into the United States.

Many of the Italian immigrants to America were from southern Italy. When American soldiers arrived in Italy during world war 2, many of there men were second generation Italians that were better educated and more successful than the northern Italians they liberated.

There is a vicious circle whereby underperformance in southern Italy leads to lack of investments, which further fuels more underperformance.

Northern Italians are known to have several derogatory terms for southern Italians considering them uneducated and rural people.

The Role of the Mafia:

The mafia is not the root cause of poverty in Southern Italy, but is rather a symptom of wider socioeconomic factors. However, it can be argued that the mafia contributes to continued under-investment and impoverishment in southern Italy. Some people would claim that the mafia is a substitute for a government in places where the legitimate government has failed.

Conclusion:

The persistent economic disparity between southern and northern Italy is a complex issue shaped by geographical, historical, and social factors. While the south possesses some fertile land and favorable ports, a lack of investment and historical circumstances have limited its economic development. Discrimination, emigration, and the presence of the mafia further perpetuate this divide. To address this disparity, concerted efforts are required to promote economic opportunities, invest in infrastructure, and foster social integration between the regions. Only through such comprehensive measures can Italy hope to bridge the economic gap and unlock the true potential of the nation as a whole.

Works Cited:

https://www.forbes.com/sites/cathyhuyghe/2022/02/28/from-silk-worms-to-prosecco-snapshot-of-northern-italian-history/?sh=2c357d615969

https://academic.oup.com/book/7358/chapter/152142375?login=false

Tags:

italy, italy economy, the economy of italy, economy, economy of italy, italian economy, the economy of italy explained, italy economy explained, brothers of italy, the economics of italy, italy's economy, italy economic crisis, italy economy economics explained, italy economic problems, economic, cons of italy, italy economics, collapse of italian economy, italy news, how italys economy works, the economy of milan, italy, southern italy, why is southern italy poor?, south italy, why is southern italy much poorer than northern italy?, why is south of italy poor, why is the south italy poor, why south italy is poor, why is southern italy not rich?, why is the north of italy so much richer than the south, difference between northern and southern italy, why is the economy of southern italy weak?, northern italy, living in italy, why is north italy richer, italy is poor

261

views

The unpleasant truth about FIRE

The unpleasant truth about FIRE

I’ve always spoken frankly and honestly to you even if the truth I speak is controversial, and sometimes upsetting. Let’s talk about FIRE. What I’m going to say is going to be hurtful to a lot of you. A lot of us do not like our jobs; in fact, we hate our jobs. The idea that you are unlikely to ever retire early is going to be frustrating.

FIRE is rich people living like poor people as a hobby. FIRE is a movement where high earners save a lot of money to retire earlier than they otherwise would have. If you are having trouble making the numbers work for you, it’s probably because FIRE is not realistic but don’t feel bad. FIRE just is not realistic for most people in most situations.

A lot of FIRE people are technology or engineering professionals that make $200k to $300k a year and retire to have a lifestyle similar to a teacher.

At the end of the day, it all comes down to your expenses. It is less about how much money you have accumulated and more about your monthly living costs. This is why so many FIRE people retire and have very modest living standards and expenses. In fact, you would be surprised how many of these people return to working.

There is an insinuation that FIRE is enabled by hard work, determination, and self-discipline. Proponents of FIRE like to consider themselves humble, hard workers, working class people. While I’m sure most of them are hard working people that are good with their money, FIRE is far more enabled through high incomes than being principled.

Studies have shown that both low income and high-income people like to consider themselves as middle income. The reality is that a median household income in the United States is about $60,000. Under these circumstances, FIRE is all but impossible. A household making $200,000 will likely consider themselves middle income, as well as working class. It will be several times easier for a high-income household to retire early in contrast to a middle income household.

The middle class has been shrinking for some time now. While America has become richer, the average American has become poorer, especially lately after you factor in inflation. There was a time that working in a factory could support an entire household, put two cars in the driveway, and pay for a nice vacation.

So, I propose we redefine FIRE as “live below your means, plans and save for the future.” You are going to need to have a decent middle-class job or dual income household to have a realistic shot at FIRE. If your household can contribute $1,000 a month to a company 401k that matches up to 6%, that is $2k per a month in retirement accounts. That should put you on a trajectory to have about $1 million in 20 years. Even that may not be enough to fire comfortably as the future is uncertain, but let’s consider this the goal for a shot at FIRE. Put away between $1,000 to $2,000, and plan for FIRE to take about 20 years.

Tags:

financial independence retire early, retire early, financial independence, how to retire early, early retirement, financial independence retire early fire, financial freedom, fire financial independence retire early, retire early fire, fire movement, fire movement retirement, fire movement explained, the fire movement, fire movement investment strategy, fire movement uk, fat fire movement, fire and movement, anti fire movement, quit fire movement, fire movement 2023, fire movement rant, slow living movement, fire movement canada, fire movement stories, zig zag movement trick, quitting fire movement, what is the fire movement, fire movement criticism, fire movement dividends, retire early fire movement

74

views

Who are the best performing investors according to Fidelity?

Who are the best performing investors according to Fidelity?

When it comes to investing, its no secret that your biggest enemy is yourself. The average person is absolutely terrible at investing. I would argue that even an above average investor still can not outperform a passively managed index fund like the S&P 500. The average investor is so bad at managing a portfolio that they have underperformed every major asset class for the last 20 years, even inflation. Therefore, the average investor would have been better off just investing in any of these asset classes and not trading in and out of positions.

That brings us to the best performing investors according to Fidelity: people that forgot they had a portfolio. Why did they do so well? There are multiple reasons. People are prone to buy high and sell low, something the reddit community WallStreetBets knows all about. Another reason is people giving into emotions like fear and greed.

I encourage you to consider just investing your money in index funds that have low expense ratios.

Tags:

stock market investing, investing for beginners, stock market, how to invest in stocks, investing, stock market for beginners, investing in the stock market, stocks, stock market investing for beginners, how to invest in stocks for beginners, stocks to buy now, dividend investing, stock investing for beginners, investing 101, stock market crash, best stocks to buy now, how to invest in the stock market, how to start investing in stocks, stocks to buy

20

views

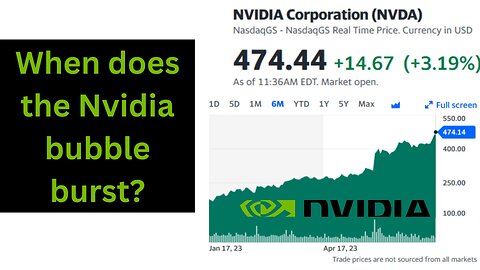

When does the Nvidia bubble burst?

When does the Nvidia bubble burst?

Nvidia’s fundamentals do not supports its current price. It can be argued that the projected revenue growth and future demand are fundamentals, and these justify its stock price. I reject that expectations have enough evidence and are grounded in reality when all things are considered.

I have seen math that shows a 27% CAGR for the next decade is priced into the stock. Nvidia would need to multiply its sales by 11 times over the next decade to justify the current stock price. This would require TSMC to increase its physical production 10 fold to meet the Nvidia demand. Nvidia will contract with TSMC to produce its next generation chips. Regardless of who manufactures the chips, whether TSMC does the vast majority of the work, or other fabs, Intel most likely, do the manufacturing, there just are not the factories present for 10 or 11 times the current Nvidia production. It takes years to bring fabs online as they are complex and heavily capital intense projects. You could refute this argument by stating the chip prices will increase because of a lack of supply, however, I would argue the price can not increase without limit. I do not see how price increases could justify an 11 times sales increase.

Let’s consider just how many data centers would have to be built to keep up with those Nvidia sales. We are talking about an insane amount of power usage to operate those data centers. You cannot deploy tens of thousands of Nvidia GPUs without spending billions of dollars on infrastructure which alone would take years to build.

If Nvidia were to miss earnings, there is a real risk the stock could fall significantly.

There is an argument that Nvidia is unstoppable at this point and the only thing that could derail the company is an anti-trust lawsuit brought by the government. However, Intel has recently entered the market, which may suggest an anti-trust lawsuit may not happen for some time. Also, congress seems unwilling to get involved with corporate consolidation in general. Intel has had issues in the past with graphics cards, and AMD seems content with taking a back seat to Nvidia, therefore making Nvidia the king of graphics cards. The mere presence of Intel and AMD may constitute genuine competition for Nvidia, or at least the perception of it that regulators and the government can cite as reasons not to go after Nvidia.

I have not been the first person to making these arguments, or reach these conclusions. Nonetheless, I can see the stock continuing to rise above $500, above $550, maybe above $600. I will continue to make these arguments, as will others. I do not see anything stopping the Nvidia stock price rising until there are issues with sales that start appearing which will trigger short selling and start pulling the stock back down to earth and reality. The market is in a state of euphoria and ecstasy when it comes to artificial intelligence and Nvidia.

Works Cited:

nvidia stock, nvidia stock analysis, stock market, nvidia stock news, nvda stock, nvidia stock predictions, nvidia stock price, stocks, stock market news, nvda stock analysis, is nvidia stock a buy, nvidia stock price prediction, nvidia, ai stocks, finance stock, best ai stocks, nvidia stock today, tesla stock, msft stock, is nvidia a good stock to buy, tech stocks, best stocks to buy now, will nvidia stock go up, nvidia stock forecast, nvidia stock earnings, stock

138

views

1

comment

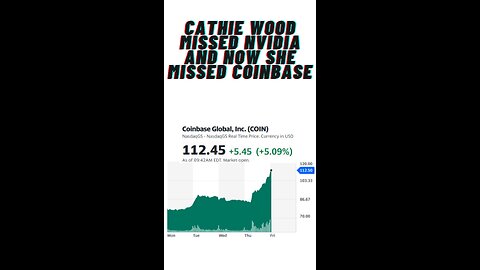

Cathie Wood missed Nvidia and now she missed Coinbase

Cathie Wood missed Nvidia and now she missed Coinbase

ARKK is an ETF that invests in “disruptive innovation” that could potentially change the way the work works. However, ARKK, and its CEO Cathie Wood, seem to continuously make bad bets and miss the most disruptive and world changing technology time after time.

I told your previously how Cathie Wood sold Nvidia stock before its enormous surge in stock price. How could ARKK and Wood not predict that artificial intelligence would need the chips Nvidia sells?

Recently, Cathie Wood sold 135,000 shares of Coinbase around the time the price hit $90.

On July 13th, a US Judge ruled that Ripple XRP was not a security. This sent Coinbase shares surging to above $110 a share. This strikes a blow to the idea that securities are being traded on exchanges like Coinbase.

Currently Coinbase is fighting the SEC over whether or not crypto assets are securities that would give the SEC jurisdiction to police them.

I would argue that the SEC has refused to work with Coinbase and other firms.

Coinbase is listed as a custodian for several spot Bitcoin ETFs, which is fueling a lot of the its share price appreciation.

Tags:

coinbase, coinbase lawsuit, coinbase sec, sec coinbase, coinbase news, coinbase ceo, coinbase sec lawsuit, coinbase vs sec, coinbase sues sec, brian armstrong coinbase, coinbase wells notice, coinbase and sec, sec vs coinbase, coinbase stock, coinbase crypto, sec sues coinbase, coinbase app, coinbase v sec, security and exchange commission, coinbase judge, coinbase vs sev, coinbase sue sec, coinbase sec news, coinbase files sec, coinbase security

81

views

1

comment

SCHD is the golden egg for dividends

SCHD is the golden egg for dividends

Or perhaps, I should say it is the standard bearer for overall dividend investing.

Schwab US Dividend Equity ETF is a passively managed ETF that tracks the Dow Jones Dividend 100 Index. It focuses on dividend paying stocks. SCHD was launched in October 2011. It is a straightforward, low cost fund offering potential tax-efficiency. It can serve as part of the core or complement in a diversified portfolio. It places an emphasis on quality and sustainable dividends. SCHD invests in stocks selected for fundamental strength relative to their peers based on financial ratios.

SCHD has a history of excellent yield and capital appreciation. It has a focus on companies with strong cashflows and return on equity. The vast majority of people will not be able to beat its returns when choosing individual stocks. Its performance resembles the S&P 500 while also providing consistent healthy dividends. While there are other ETFs like JEPI that beat it on the basis of yield, their long-term performance just does not compare. It is a fool’s errand to chase yield alone as this results in underperformance.

In general, ETFs are safer than individual stocks. A dividend ETF is arguably the safest and most reliable ETF you can purchase.

The biggest selling point to me is the razor thin expense ratio of 0.06%.

However, I recognize that there is an argument to be made against SCHD. If we look at VOO, Vanguard 500 Index Fund ETF, it slightly outperforms SCHD, however SCHD is more stable and pays reliable dividends. VOO has a relatively low yield of less than 2% because it holds companies that don’t pay dividends, thus lowering the overall yield. However, this index has a track record of over 100 years and an average annual return exceeding 9%. Therefore, it can be argued that it is potentially safer and more diversified than SCHD. We also must keep in mind that share buybacks are more cost-effective in returning value to shareholders than dividends.

I would counter that SPY has more volatility than SCHD. The S&P 500 holds a significant amount of growth and technology companies. In contrast, SCHD is more defensive. SCHD contains about 100 companies.

SCHY is the international version of SCHD, but the expense ratio is significantly higher at 0.14%.

If you are a dividend investor, I would strongly encourage you to look into SCHD.

Works Cited:

https://www.financialtechwiz.com/post/voo-vs-schd

https://money.usnews.com/funds/etfs/large-value/schwab-us-dividend-equity-etf/schd

https://www.schwabassetmanagement.com/resource/schd-fact-sheet

Tags:

schd, schd etf, schd dividend, schd etf review, schd vs voo, schd review, schd 2023, retire off schd, schd vs jepi, schd dividend etf, schd 2022, schd dividends, schd vs vti, schd vs vym, schd divdiend etf, schd dividend growth, dividend investing schd, schd stock, schd etf review 2023, schd etf 2023, how much to live off schd dividends, why schd is down, schd etf reveiw, buy schd, schd etf dividend, schd down, 2023 schd, schd dividend review

91

views

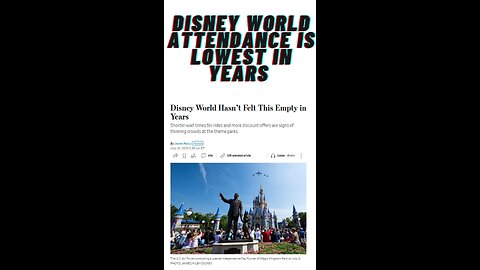

Disney World attendance is lowest in years

Disney World attendance is lowest in years

Could this be the result of price hikes? Or are there larger issues at play?

Independence Day weekend was the slowest one in nearly a decade.

Disney is now offering hotel discounts during Christmas, which is a peak period, signally trouble.

Disney has suffered losses with its streaming platform, Disney+. In addition, there has been turmoil with its CEO and executive succession as well as a political and legal fight with the Governor of Florida.

Revenue from the parks division is crucial to buoy up the overall earnings. The price hike by Disney was intentional to squeeze cash out of visitors, as well as thin out crowds. The cost of a two day ticket has increased over 11% from $255 per an adult to $285.

However, pent up travel demand may be going towards cruises and Europe instead of Disney.

Disney doesn’t have any new attractions opening soon except a reimagination of Splash mountain at both Florida and California parks. In addition to price hikes, they slashed free amenities.

Works Cited:

https://www.wsj.com/articles/disney-world-crowds-universal-studios-florida-36b0a579?mod=hp_lead_pos7

Tags:

disney stock, disney stock analysis, stock market, dis stock, disney stock news, is disney stock a buy, stock market news, stocks, disney, disney stock forecast, dis stock analysis, disney stock predictions, disney stock 2023, disney stock today, disney stock review, stock, is disney stock a good buy, disney stock price prediction, stocks to buy now, finance stock, disney stock price, disney stock earnings, disney plus, is disney stock a good buy 2023

36

views

What will happen if interest rates fall below 3% or 4%?

What will happen if interest rates fall below 3% or 4%?

The most prominent thing would be that everyone with an interest rate of 5% or greater would refinance.

However, any decrease in interest rates will be the result of Quantitative Easing. QE would the response of the government to try and stimulate the economy.

Many people are eagerly waiting for a housing market crash that will give them the opportunity to purchase real estate at bargain prices. A housing crash is almost always in tantum with a wider economic recession. The issue people ignore is what they will do for income if there is an economic recession. Rooting for disaster is based on the false pretense that you will be left unscathed and fully able to liquidate your savings to purchase a house. What job will be left untouched by an economic catastrophe? A popular rebuttal to this argument is that unemployment was only about 10% during 2008 which suggests only 1 in 10 people were impacted by the recession. However, I would argue the majority of people were negatively impacted, especially people in cyclical and discretionary industries like construction, entertainment, dining, and retail. It is likely that the people that can’t afford a house now would be the most impacted by any sort of economic turbulence.

Tags:

mortgage rates, mortgage interest rates, mortgage rates 2023, mortgage rates today, best mortgage rates, interest rates, mortgage rates forecast, mortgage rates forecast 2023, mortgage, , mortgage rates rise, mortgage rates jump, mortgages, mortgage rates explained, mortgage interest rates today, mortgage rates predictions 2023, mortgage guidelines, high mortgage rates, mortgage rates 2024, interest rates, mortgage interest rates, mortgage rates, high interest rates, raise interest rates, rising interest rates, interest rate hike, interest rates latest news, interest rate, us interest rates, fd interest rates, fed interest rates, latest news, cuts interest rates, interest rates news, interest rate rise, interest rates on hold, rates, what are interest rates, federal interest rates, interest rates mortgage, interest rates no change, interest rate rises

136

views

Why is bar soap cheaper than body wash?

Why is bar soap cheaper than body wash?

1) Packaging: The cost of packaging is a significant driver of body wash. The cost of packaging is often more expensive than the contents of many consumer products. Bar soap packaging is usually less elaborate, often taking the form of just a cardboard box. In contrast, body wash usually comes in plastic bottles and may feature a pump.

2) Transportation and Storage: With bar soap, you are not paying for water weight which inflates the cost of soap in terms of how much you can fit in a box at the warehouse, and how many of those boxes can hit on a truck. In fact, most of the liquid soaps and body washes are water. In addition to the space to store and transport, there is also the risk of spillage and broken containers.

3) Marketing and Advertising: There used to be commercials perpetrating to show all the bacteria supposedly harbored on bar soap which resulted in a misperception that bar soap was somehow dirty. This is nonsense because soap is inherently antibacterial. Bar soap is considered for poorer people while body wash is considered a luxury. There is a higher profit margin for body wash, which can justify spending more on marketing and commercials. These costs are passed on to the consumer.

4) Ingredients: Bar soaps usually are made from fats and sodium hydroxide. When sodium hydroxide reacts with fats, it creates the active ingredient sodium stearate. The issue with sodium stearate is that it does not work well with hard water which may cause it to leave deposits on the skin after being washed, potentially clogging pores and making your hair feel heavy. Body washes usually contain synthetic detergents which do not cause as many issues when combined with hard water.

On a personal note, I like Dove “beauty bars” which technically can’t be labeled as soap. They have extra moisturized added and are gentle on your skin. They are a mild cleanser and contain about 25% moisturizing cream. They are a relatively simple formula, and are therefore quite affordable.

Tags:

bar soap vs body wash, bar soap, body wash, body wash versus bar soap, does bar soap or body wash clean better, is bar soap better than body wash, bar soap vs body wash environment, bar soap or body wash for dry skin, soap, best bar soap for men, best bar soap, bar soap and body wash, bar soap body wash, which cleans better bar soap or body wash, bar soap vs body wash men, bar soap versus body wash men, bar soap or body wash, bar soap and body wash men

42

views

Should you have an airline credit card?

Should you have an airline credit card?

An airline credit card may or may not make sense for you and your family. Today we are going to discuss situations where it would and would not make sense to get one based on factors that include airline loyalty, rewards, annual fees, credit card usage, and additional features.

The perks of an airline credit card include large sign-up bonus, free checked bags, and access to airport lounges.

Many frequent fliers already earn status with an airline. These travelers already get the same perks without airline credit cards. Frequent fliers would be better served with rewards other than those focused on flying. For example, frequent fliers often already get a free checked bag. Many airline credit cards have annuals fees between $100 to $550. Redundancies in rewards create monetary waste. In contrast to frequent flyers, a family of four that only flies once a year could more than pay for the annual fee of an airline credit card with one trip.

Before the pandemic, fliers built up vast reserves of airline points and miles. Now that everyone is traveling again, people are eager to spend these points and miles. In response, airlines have begun to raise prices and ratchet up the miles and points required to book a flight. Miles and points are not going as far as they once did.

It’s important to remember that booking a flight with miles or points does not make it free as you still need to pay for taxes, fees, and surcharges which can add up to hundreds of dollars.

Some airlines like Alaska Airlines offer better bonuses depending on the time of year or even the market you are in. For example, Alaska Airlines has targeted small business owners in Boise, Idaho in the past.

Most airline credit cards highlight lounges which may feature perks like free food and drinks, nice seating, free Wi-Fi, and even showers or nap pods. However, lounges have increasingly become so crowded at major airports that there are sometimes lines just to get in.

Ask yourself would you pay for a given benefit before you sign up for a credit card just to get it.

Some airline credit cards automatically qualify the cardholder to a higher level of status within the frequent flier program which could mean upgrades or early boarding.

Some airlines feature a companion pass whereby you can purchase an additional ticket for a companion at a reduced rate or even for free.

One strategy is to have multiple travel orientated credit cards. One card would be with an airline for its ancillary benefits. Another would be with a bank to earn points for travel.

Perhaps the easiest route is to just get a 2% unlimited cash back credit card and use it to pay for everything. Then, get a credit card for the airline that dominates your local market and use that for travel. A round trip’s bag fees should pay the annual fee on that card.

Some notes and observations:

Some people would say that American Airline’s frequent flier miles are worth something in contrast to Delta.

Some people would argue that miles directly with most airlines have become worthless unless you are flexible and willing to overnight on a layover when you can’t find a flight.

Works Cited:

https://www.wsj.com/articles/airline-credit-card-perks-frequent-flier-miles-7bc224c8?mod=hp_featst_pos4

Tags:

best credit cards, credit cards, airline credit cards, credit card, best credit cards for travel, travel credit cards, best credit cards 2023, best airline credit card, best travel credit card, airline credit card, chase credit cards, credit cards 101, credit card points, american airline credit card, best credit cards 2022, american express credit cards, alaska airlines credit card, credit score, best airline credit cards, amex credit cards

116

views

What is an 80/20 budget??

What is an 80/20 budget?

The 80/20 budget divides your take home income from your pay into two spending buckets:

1) need & wants

2) savings

This technique is also known as the “pay yourself first” budget.

When you get your paycheck, you will first put 20% of your income away in savings, then the 80% that remains will go towards paying off everything else. By putting 20% away for savings right away, the priority is savings money. With the remaining 80%, it is best to pay off the essentials first like rent and utilities.

The 20% of your savings should be directed at tax advantaged retirement accounts like IRAs and 401(k)s. If you employer matches your 401k contributions, of course you want to max that contribution out. Once you have maxed out your employer match, you should make sure you have an emergency fund in case you lose your job or your car breaks.

The 80/20 budget is easy to use and simple which makes it great for beginners.

Tags:

how to budget, budget, 50 30 20 budget, what is a budget, 50/30/20 budget, 50 30 20 budget rule, how to make a budget, 80/20 budget, 80/20 budget rule, how to budget money, 80/20 rule, how to create a budget, 70 20 10 budget, what is the best budget rule, budget tips, create a budget, save money with a budget, how to budget and save money, how do i budget, how to save money with a budget, how to stick to a budget, 80 20 budget, budget my money

35

views

Do I need title insurance?

Do I need title insurance?

Owner’s title insurance protects you, the property owner, against financial losses related to defects or issues with the property title. While rare, these defects and issues with the title can be potentially devasting and ruin you financially. Owner’s title insurance policies help pay for legal fees, court costs, and any financial losses incurred by the property owner.

Always get title insurance.

What you want is a clear and marketable title that allows you the legal right to own and sell property without any encumbrances or disputes.

Despite even the most thorough research and examination of a property’s title history, there can still be issues that arise after purchase. An owner’s title insurance will protect you from a potentially devasting loss.

Common property title risks include:

1) Errors and omissions in the public records made during the recording or indexing of documents. These mistakes range from incorrect legal descriptions, misspelled names, or incorrect property boundaries.

2) Undisclosed liens or encumbrances. Liens are placed on a property for unpaid taxes, mortgages, judgments, and other debt. Owner’s title insurance can protect you from surprised discovered after the purchase.

3) Forgery or fraud as a result of someone forging documents to affect the property’s title or transfer ownership.

4) Unknown / missing heirs in cases where there is someone who may have a claim to the property but was not properly identified or notified during the title search.

5) Invalid or improperly executed documents that affect the title.

Lender’s title insurance is for the bank. It is insurance on your loan and doesn’t benefit you. Lender’s title insurance is completely different than owners title insurance. The lender is not going to protect you from title theft, errors, and property disputes. Banks require you to purchase lender’s title insurance but an owner’s title insurance will likely be optional. However, if you are working with a real estate lawyer, I would wager they make you purchase it as a condition of working with them.

If you ask a title insurance agent, they will tell you that they find errors on a regular basis. The people processing real estate documents make mistakes. Title insurance also helps in case there is fraud.

You should still opt to get title insurance even when you refinance. Errors may be found in the original closing during the refinance title reviews. More often than not it pertains to bad legal descriptions. The new lender will require a loan policy insuring themselves.

The old title insurance policy only insurers against events up to the date of the policy. Nothing after that. The new policy covers anything that may have happened after that, up to the date of the new policy.

A title insurance claim indicates that there was a mistake on the part of the title insurance company. A title insurance company has almost complete control of the insured risk through the scope of their work, and therefore, if they do a proper job, they will have few insured claims.

Title insurance is more important on new construction than on existing residential property.

In most states, owner’s title insurance policies do not cost very much because they only charge on the difference between the value of the mortgage and the value of the home.

My advice to you is always get owner’s title insurance.

Tags:

title insurance, what is title insurance, owners title insurance, title insurance real estate, title insurance explained, owner's title insurance, title insurance policy, lenders title insurance, is title insurance required, owners title insurance explained, title insurance definition, title company, title insurance cost, why title insurance, title insurance 101, do i need title insurance, what does title insurance cover, title, what is title insurance and do i need it?

62

views

Are target date funds bad?

Are target date funds bad?

Target date funds gradually shift their asset allocation over time to become more conservative as the target date approaches. The target date refers to the date of anticipated retirement. For example, a 2050 fund would be for those targeting to retire in the year 2050. The fund seeks to maximize returns and minimize risk based on the time horizon.

Target date funds are a popular tool. They are perhaps best compared to one size fit all clothing: they fit the average person well but your milage will vary.

They are a blend of investments designed for a certain timeline. They progress from more aggressive to more conservative over time. They are a fine choice for people that do not want to micro-manage their portfolio and asset allocation, instead, preferring a hands-off approach that emphasizes convenience and simplicity.

They are best suited to tax advantaged portfolios like a 401k or IRA because they rebalance regularly. The rebalancing of the fund creates capital gains distributions. There is also interest from bonds held in the fund that is taxable as ordinary income. They are not tax efficient, and therefore should not be held in a taxable brokerage account.

There is substantial evidence that actively managed accounts trail passive, diversified, low cost options like target date funds, especially after fees and expenses. I would argue target date funds are preferable to active management that is often quite costly. Not only can you have better returns by not picking individual stocks and instead relying on a target date fund, but you can also save yourself a lot of time and stress. I’d say if a target date fund keeps you from going in and out of stock positions, put your money in a target date fund.

Not all target date funds are going to be passively managed with a low expense ratio. The Schwab Target 2055 Fund (SWORX) has an expense ratio of 0.58% versus the Schwab Target 2055 Index Fund (SWYJX) with an expense ratio of 0.08%.

However low expense a target date fund is, it is still more expensive than the sum of the individual pieces. For example, VTTSX has an expense ratio of 0.08% but the individual funds it invests in have a combined expense ratio of ~0.04. On a $100,000 that is $40 per a year. For a million dollars, that is only $400 per a year. Therefore, the added expense of a target date fund versus the sum of the individual components is negligible, I would argue.

One of the main issues I have with them is that they tend to be overly conservatives. The solution to this issue is picking one that is 5 or 10 more years out.

Works Cited:

https://www.investopedia.com/terms/t/target-date_fund.asp

Notes:

The difference between a 90/10 stock/bond allocation and a 100/0 is not much in terms of performance, but there is a large difference in terms of risk.

Tags:

target date funds, target date funds explained, target date fund, fidelity target date funds, target date funds vs index funds, vanguard target date funds, best target date fund, target date, investing in target date funds, 401k target date funds, vanguard target retirement funds, what are target date funds, target date funds vanguard, target date funds pros and cons, target date index funds, target date retirement funds, target date fund for retirement

114

views

What happens if you get sued for more than your policy limit?

What happens if you get sued for more than your policy limit?

Your insurance is likely going to hire an attorney if you are being sued for something related to your insurance like a dog bite or an automobile crash. The attorney will deal with most everything. However, you may get a letter from the insurance that there has been a court filing above what your liability coverage is in your policy.

While it is likely that the case will settle within the policy limits, but that is not a guaranteed outcome. When a lawsuit is filed that exceeds your policy limits, you do need to be informed. If the ultimate judgement is over the policy limits, you would then have personal liability.

There is a reason that many renter’s insurance policies are so cheap. They do not always have good coverage.

Make sure you double check your insurance coverage and make sure you have the correct limits. Also, consider umbrella coverage. It will be cheaper than you think it is.

Tags:

insurance, policy limit, car insurance, insurance claims limit, policy limit demand, insurance policy components, insurance policy limits, auto insurance, home insurance, illinois insurance policy limits, insurance limit, renters insurance, what is insurance policy, business insurance, policy, policy limit gap, how do insurance policy limits affect car accident cases, medical insurance, life insurance, term insurance, components of insurance policy, lawsuit, injury lawsuit, league city police lawsuit, personal injury lawsuit time limit, filing a lawsuit, personal injury lawsuit, lawsuits, insurance claims limit, lawsuits and the role of insurance, difference beteen an insurance claim and a lawsuit, million dollar lawsuit, difference between an insurance claim and a lawsuit, difference between an insurence claim and a lawsuit, 1 million dollar lawsuit, multi million dollar lawsuit, lawsuit timeline, retaliation lawsuit

28

views

Why is manufacturing construction spending so high?

Why is manufacturing construction spending so high?

In May 2023, there was 194 billion in construction spending in the United States.

This is primarily a semiconductor, computer, and electrical related manufacturing investment being driven by the CHIPS Act, which includes batteries. This sector was a relatively small share of manufacturing construction in the past decades but now it is the dominant component.

This government backed demand to build chip fabrication plants, battery plants, and renewable energy facilities is fueling construction spending for the manufacturing industry. You also have companies that are leaving China to de-risk and diversify manufacturing.

It is important to adjust for price increases because construction costs have risen sharply in recent years. Nominal spending should not be misconstrued for increased physical construction.

The boom in the computer / electronic segment has not been offset by reduced spending on other segments which have been largely consistent over time.

Works Cited:

https://home.treasury.gov/news/featured-stories/unpacking-the-boom-in-us-construction-of-manufacturing-facilities

Tags:

construction spending, construction, us construction spending, construction spending rises, construction (industry), u.s. manufacturing rebounds; construction spending falls, us construction, u.s. construction, 2022 construction, construction cosmos, construction insurance new jersey, consumer spending, us manufacturing construction, construction materials, construction technology, new jersey construction insurance, construction materials (trbc), spending rises

98

views

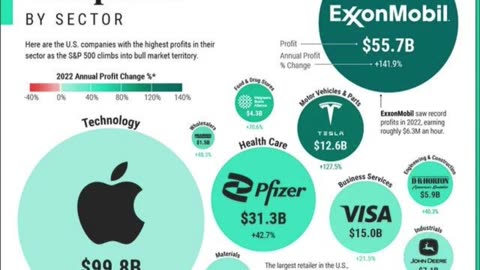

What are the most profitable companies by sector?

What are the most profitable companies by sector?

Apple is the most profitable company in the world with a 43% gross margin in Q1 2023. Apple can charge a premium price for its products because they are of high quality and innovative. While the iPhone is the biggest source of revenue, the most profitable business segment is service. The 2022 net margin was 25.31%.

ExxonMobil is the most profitable energy company, reporting $55.7 billion in 2022 profit. The amount of profit dollars more than doubled since the prior year driven by increased oil and gas output. The 2022 net margin was 13.92%.

JPMorgan Chase is the most profitable financial company with $37.7 billion in 2022 profit. Despite home lending being down, banking and wealth management was up, as well as corporate and investment banking. The 2022 Net Margin was 23.79%

Pfizer is the most profitable health care stock with $31.3 billion in 2022 profit. The largest driver of profit last year was the COVID19 pandemic. The company sold almost $40 billion in vaccines. Gross profit was 61.89% in 2022.

Home Dept is the most profitable retailer with $17.1 billion in profit dollars last year. The largest revenue segment is indoor garden at 9.5%, followed by appliances at 9.2%. The net margin last year was 10.9%.

Tags:

most profitable companies, profitable business ideas, the most profitable companies in india in 2023, most profitable businesses, most profitable industries, top most profitable companies, most profitable companies 2023, sim companies most profitable, india's most profitable companies of fy23, most valuable companies in the world, most valuable companies, most profitable industries in the world, most profitable industries in the us, most profitable companies in the world

16

views

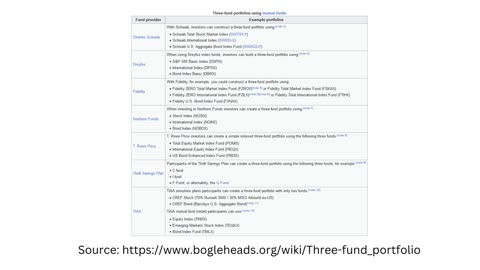

What is a Three-Fund Portfolio?

What is a Three-Fund Portfolio?

A three-fund portfolio is a simple investment strategy to maximize your portfolio’s return. The three-fund portfolio is renowned for its simplicity, tax efficiency, diversification, and low-cost. Perhaps the simplest strategy is to put all your money in a target-date fund. It is mathematically certain to out-perform most investors. If you want a little bit more elaborate of a set up than just plowing all your money into a target date fund, this is just one step up in complexity.

The three-fund portfolio is comprised of three pieces that should be low-cost and representative of the entire market:

1) Domestic stocks – usually a total stock market index fund

2) International stocks - International stocks provide diversification from US stocks.

3) Domestic bonds – Bonds are low risk, low reward. They are a relatively safe investment. As you approach retirement, you will want to increase your exposure to bonds.

Advantages

Investing is a compromise between simplicity and control. The three-fund portfolio offers a middle ground between the simplicity of a target-date fund, and the complexity and time consuming work of investing in individual stocks.

The three-fund portfolio prioritizes diversification which is a fundamental concept of investing.

Your investing horizon would determine the allocation of your portfolio. The more time you have to invest, the more weight you would put into stocks.

Works Cited:

https://www.bogleheads.org/wiki/Three-fund_portfolio

https://www.investopedia.com/3-fund-portfolio-401k-5409269

Tags:

three fund portfolio, 3 fund portfolio, lazy 3 fund portfolio, 3 fund etf portfolio, 3 fund portfolio vanguard, boglehead 3 fund portfolio, 3 fund portfolio fidelity, bogleheads 3 fund portfolio, bogleheads three fund portfolio, 3 fund investment portfolio, boglehead portfolio, vanguard 3 fund portfolio, three fund portfolio 2023, 3-fund portfolio, bogle three fund portfolio, 2 fund portfolio, is a three-fund portfolio right for you?, 3 fund portfolio allocation

30

views

What is the Waffle House Index?

What is the Waffle House Index?

Waffle House is a restaurant chain that is known for being open 24/7. It is rarely ever closed except when there are severe weather events. For this reason, it is used as an informal gauge by FEMA to assess the impact of a natural disaster. The phrase “Waffle House Index” was coined by a FEMA administrator in 2011 following the Joplin EF5 tornado that left 158 people dead and caused $2.8 billion dollar in damages. Despite this, two Waffle House restaurants remained opened.

The index has three levels

1) Green: full menu – The Waffle House has power and water and damage is minimal or absent

2) Yellow: limited-menu – The Waffle house is either has no power, or power is being delivered by a generator. The Waffle House may or may not have water. Food supplier are running low.

3) Red: closed – The Waffle House has been severely damaged or flooded.

Works Cited:

https://www.wafflehouse.com/how-to-measure-a-storms-fury-one-breakfast-at-a-time/

Tags:

waffle house, waffle house index, waffle house meme, waffle house menu, waffle house lore, waffle house host, waffle house index map, the waffle house index, waffle house chair video, waffle house new host, waffle house index 2023, waffle house index explained, what is the waffle house index, waffle house has found its new host, is there a real waffle house index, waffles, waffle, waffle house wendy, waffle house video, waffle house scp, the waffle house

59

views

Are dividend stocks only for older people?

Are dividend stocks only for older people?

Most dividend stocks have low betas, which I will define as anything less than 1.0. Let’s talk briefly about betas, and then talk about how they relate to dividend stocks, and what you should be considering for your investments.

Beta is used to measure a stock’s risk. It is a measure of a stock’s volatility in relation to the overall market. Something that mirrors the S&P 500 Index exactly would have a beta of 1.0. A stock that amplifies the swings of the market will high a beta above 1.0. A stock that swings less than the market does will have a beta less than 1.0.

Higher beta stocks are supposed to be riskier but provide higher potential returns. In contrast, a low beta would be associated with less risk and less return.

Dividend stocks are going to have lower betas. They are good for capital preservation and stability, but offer less potential growth in the form of capital appreciation. So theoretically, low beta stocks might be better for older people that are closer to retiring. Older people are going to have more money than young people. If you have half a million in dividend stocks maybe 3% dividends, that is $15,000 in dividend payments each year. The older you get, the more defense you want to play your investments. The name of the game becomes capital preservation rather than appreciation. While dividend stocks are particularly attractive for older people, I would argue that they are for everyone, even young people. The major online brokerages all have some type of dividend ETF, and I own some of these in my own portfolio. Don’t write off dividend stocks as just for boomers. These investments might be as sexy and environmentally friendly as Tesla, but they are consistent and steady which means something.

There are tax considerations for dividend stocks that I would be remiss if I didn’t mention. Taxes will have an impact because if you are paying taxes in dividends, that is money that is not working for you in the stock market, it’s going out of your pocket to the tax authorities. That dollar you just paid in tax could have been generating returns in the stock market for decades until it was time for you to cash out. Therefore, there is an argument that capital gains are better than dividends. However, dividends are tax free in Roth 401(K) and you will not pay taxes in a traditional 401(k) until you start making withdrawals, which should be in retirement.

Growth stocks, like technology, are going to have higher betas. They should outperform the market over a longer time frame and are better for younger people with longer time horizons. However, you can’t invest just based on betas. That would lead you to invest in companies that are risky and may have less financial health. You could quickly go broke just focusing on high betas alone.

In the end, you really can’t go wrong investing in an S&P 500 index fund or a total market index fund. Also, be sure you portfolio has a bit of international exposure so you are better diversified.

Tags:

dividend investing, dividend stocks, dividend growth investing, best dividend stocks, dividend income, dividend portfolio, investing, dividends, dividend stocks to buy, top dividend stocks, investing for beginners, dividend investing strategy, best dividend stocks 2023, dividend, the power of dividend investing, dividend growth, monthly dividend stocks, dividend investing portfolio, dividend investing for beginners, live off dividends, dividend growth stocks

53

views

Why you should use an independent insurance broker

Why you should use an independent insurance broker

You are going to feel silly you never used one before and you will never go back to the old way.

Independent insurance brokers work with multiple insurance companies which gives you access to a wide range of options. They will make it easy to compare coverage, premiums, features, etc.

As you get older and make more money, and have more things, maybe a boat or jet ski, or a motorcycle, you situation is going to become increasingly more complicated. A broker is going to be able to give you personalized advice and guidance. People are either way underinsured, or way too overly insured. A broker is going to assess your risks and explain policy details to you.

Perhaps the coolest thing is that a broker can help you advocate for yourself and deal with claims. They can act as a liaison between the insurance company and you.

If you use a broker, you can avoid the hassle of shopping around for insurance.

As your life and financial situation changes, the broker can continue to tailor your policies to you.

Best of all, you will probably save money. It’s a myth that using a broker will result in paying more money overall.

Tags:

insurance broker, independent insurance agent, independent insurance agency, insurance agent, insurance, life insurance, independent medicare insurance broker, how to sell insurance, insurance agent training, independent insurance, insurance career, independent insurance broker, insurance broker vs agent, become an independent insurance agent, independent medicare insurance agent, independant insurance broker, why use an independent insurance broker

17

views