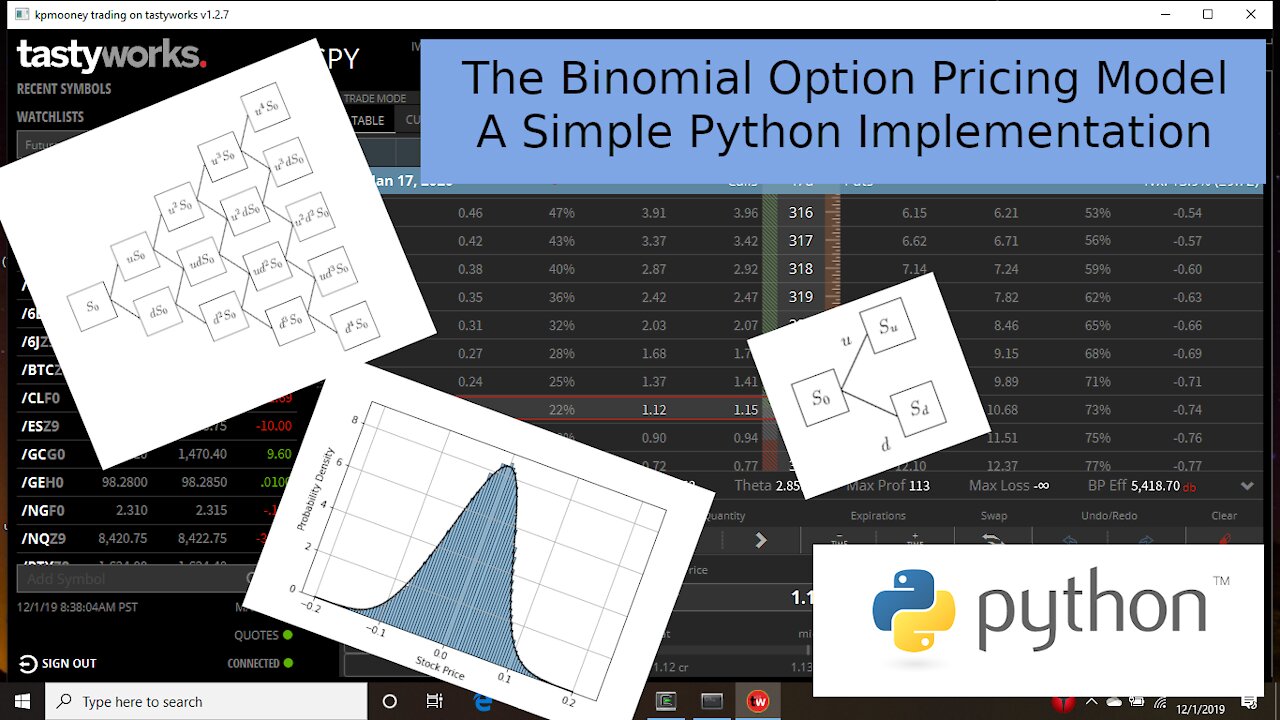

Implementing the Binomial Option Pricing model in Python

4 years ago

53

We will implement a simple binomial option model in Python. A binomial model assumes a stock moves discreetly either up by a specified percentage or down by a specified percentage. The “binomial” here refers to the fact there are only two possible values for the stock to take on in any given time step. Options are then priced based on the resulting tree-like structure working back from expiration to the time of interest.

Tip Jar: https://paypal.me/kpmooney

Loading comments...

-

22:17

22:17

kpmooney

4 years agoImplementing the Bachelier Option Pricing model in Python (Part 1)

196 -

15:13

15:13

kpmooney

4 years agoImplementing the Bachelier Option Pricing model in Python (Part 2)

29 -

14:53

14:53

kpmooney

4 years agoGenerating Option Payoff Plots in Python

108 -

21:36

21:36

kpmooney

4 years agoCalculating Implied Volatility from an Option Price Using Python

134 -

11:24

11:24

kpmooney

4 years agoCalculating the Implied Volatility of a Put Option Using Python

9 -

9:50

9:50

kpmooney

4 years agoCalculating Implied Volatility from an Option's Price Using the Binomial Model

67 -

2:24

2:24

WSYM

4 years agoAffording Care, Membership Model Becoming A More Popular Option

7 -

0:19

0:19

Tony Go Wild

4 years ago $0.01 earnedGOLD PYTHON - Albino Python Snake

82 -

10:43

10:43

normanfenton

4 years agoBinomial Distribution

27 -

14:02

14:02

pcomitz

4 years agopython functions

106