Implementing the Bachelier Option Pricing model in Python (Part 1)

4 years ago

196

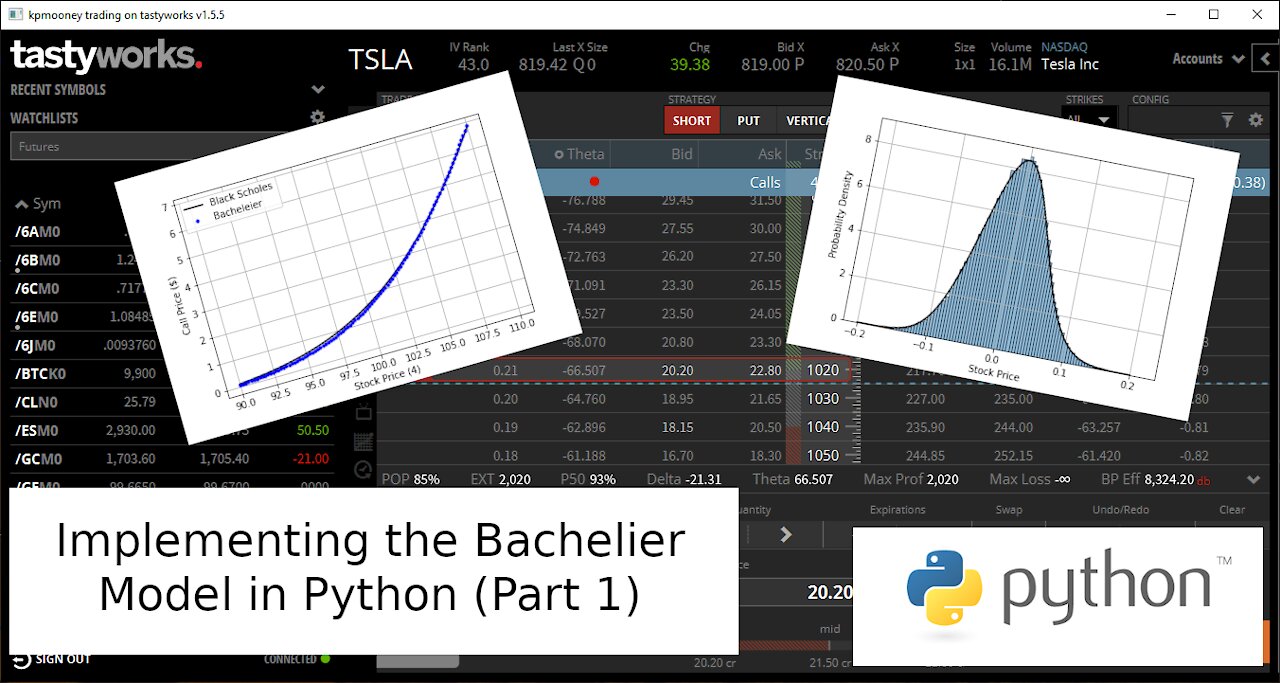

I recently received a question about the Bachelier model, a historical model from around 1900. It has regained some use as of late, with the CME using it since it allows for negative commodity prices. In this video, we’ll build out a Python function to return the Bacheleier price of a call. We’ll then compare this to the Back Scholes model. Lastly we will show to to numerically calculate the greeks associated with this model and use vega to calculate the volatility given the price of a call.

Tip Jar: https://paypal.me/kpmooney

Loading comments...

-

15:13

15:13

kpmooney

4 years agoImplementing the Bachelier Option Pricing model in Python (Part 2)

29 -

14:53

14:53

kpmooney

4 years agoGenerating Option Payoff Plots in Python

108 -

21:36

21:36

kpmooney

4 years agoCalculating Implied Volatility from an Option Price Using Python

134 -

11:24

11:24

kpmooney

4 years agoCalculating the Implied Volatility of a Put Option Using Python

9 -

8:16

8:16

kpmooney

4 years agoSolving Banded Linear Systems in Python (Part 4)

32 -

2:24

2:24

WSYM

5 years agoAffording Care, Membership Model Becoming A More Popular Option

7 -

17:46

17:46

kpmooney

4 years ago $0.01 earnedNumerically Solve Boundary Value Problems: The Shooting Method with Python (Part 1)

114 -

14:02

14:02

pcomitz

4 years agopython functions

106 -

4:27

4:27

pcomitz

4 years ago $0.02 earnedInstalling python

243 -

40:12

40:12

kpmooney

4 years agoDifferential Equations and Maximizing Functions in Python: Solving Simple Physics Problems (Part 1)

41