Numpy and Scipy: Using Sparse Matrices to Speed up Calculations (part 1)

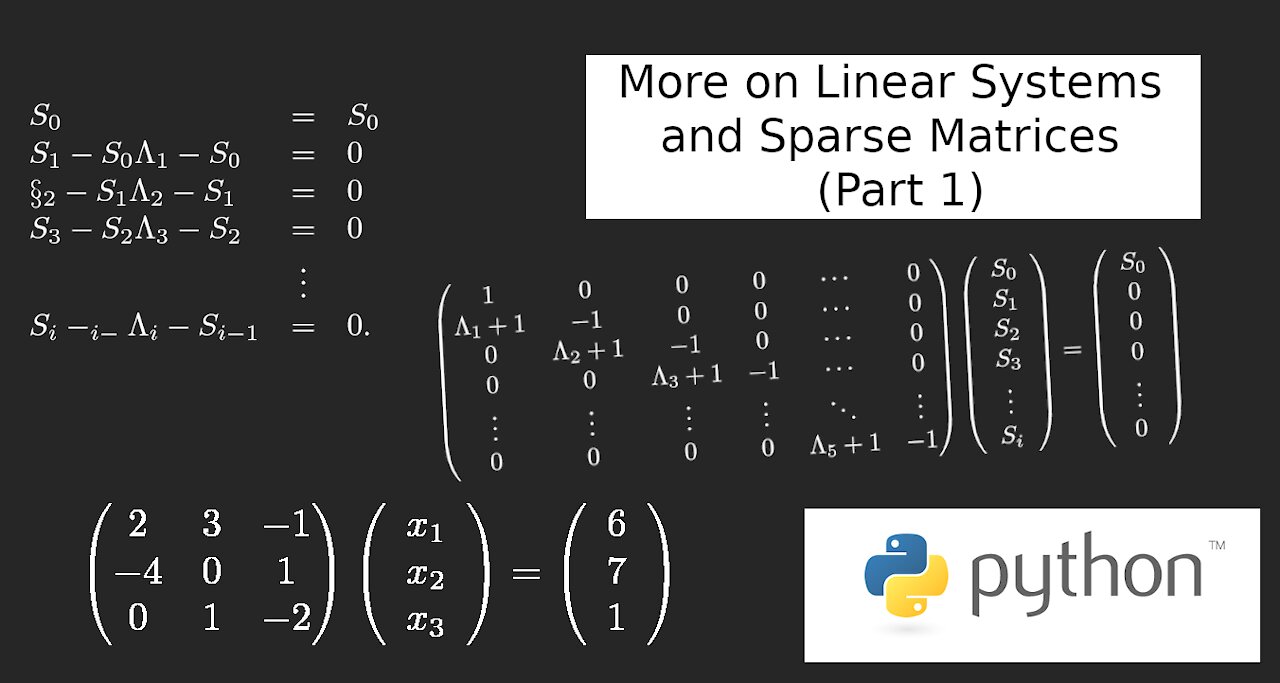

In response to a comment on the videos dealing with Monte Carlo models of stocks market movement, and how to calculate the probability of making 50% of max profit on an options trade, I want to revisit some of the concepts presented in those videos. In particular the concept of linear systems which can be represented by matrix equations where the coefficient matrix is sparse. I will go through the calculations used in these videos and show, step-by-step, how the matrices involved are generated. This will be part one of three where we show how sparse matrices and linear algebra are used to speed up calculations. Part two will deal with solving a partial differential equation. Part three will return to to the matrices used in the Monte Carlo calculation.

Probability of making 50%: https://youtu.be/yGlkRpqMDVk

Probability of a Touch: https://youtu.be/PRLnusDWSW0

Tip Jar: https://paypal.me/kpmooney

-

13:06

13:06

kpmooney

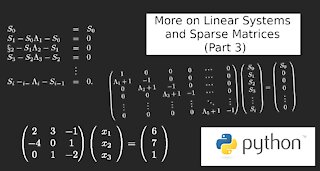

4 years agoNumpy and Scipy: Using Sparse Matrices in our Monte Carlo Simulation (part 3)

8 -

29:48

29:48

kpmooney

4 years agoSparse Matrices to Speed up Calculations (Part 2): Partial Differential Equations - 1-D Diffusion

43 -

20:38

20:38

kpmooney

4 years agoLinear Systems and Sparse Matrices with Numpy and Scipy

64 -

27:14

27:14

kpmooney

4 years agoTransforming Ordinary Differential Equations to A simple Algebraic System Using SciPy (Part 1)

341 -

18:45

18:45

kpmooney

4 years agoTransforming Ordinary Differential Equations to A simple Algebraic System Using SciPy (Part 2)

251 -

1:42

1:42

Gta_Stash

5 years agoGTA 3 - stunt jumps on car, using 'CORNERSLIKEMAD' cheat (part 3)

50 -

2:05

2:05

Gta_Stash

5 years agoGTA 3 - stunt jumps on car, using 'CORNERSLIKEMAD' cheat (part 2)

35 -

0:46

0:46

STLNutritionDoc

4 years agoSpeed bag

22 -

0:06

0:06

tboi86

4 years ago $0.01 earnedSpeed Training

65 -

0:50

0:50

3D animations and CGI

4 years agoPanasonic GH5 Sample Videos using Canon 28-135 Ultrasonic Lens with Viltrox Speed Booster

112