life and accident insurers that have already paid claims could take aggressive legal action through

XIXI ASKED DEEPSEEK:

Assume that 70% of Acorn's stairlifts have currents on touchable surfaces that exceed regulations or codes, and the 20,000 or so deaths and injuries found by Akkio and ZERLO AI hidden in regulatory and Hindle Institute databases are accurate, what could life and accident insurers do, with subrogation rights, after these insurers had paid out?

DEEPSEEK ESTIMATED::

If 70% of Acorn stairlifts have dangerous electrical currents on touchable surfaces, leading to 20,000+ deaths/injuries (as uncovered by Akkio, ZERLO AI, and Hindle Institute data), life and accident insurers that have already paid claims could take aggressive legal action through subrogation to recover losses. Here’s how:

Subrogation Strategy for Insurers

Insurers can sue responsible parties to recover payouts made to victims. Potential targets:

A. Acorn Stairlifts (Manufacturer)

- Claims:

- Defective design (excessive current leakage).

- Failure to warn (ignoring IEC 60601-1, NEC 70, or EU Low Voltage Directive).

- Fraudulent concealment (hiding safety violations in regulatory filings).

- Legal Theories:

- Product liability (strict liability, negligence, breach of warranty).

- Punitive damages (if misconduct is proven).

B. Installers & Contractors

- Claims:

- Negligent installation (failed to test for leakage currents).

- Code violations (ignoring GFCI/grounding requirements per NEC 210.8).

- Example Case:

- Estate of Rodriguez v. Home Depot (installer liable for non-GFCI outlet death).

C. Regulatory Bodies & Testing Labs

- Claims (if applicable):

- Negligent certification (e.g., if UL/TÜV approved defective units).

- Failure to recall (if regulators ignored whistleblower data).

D. Property Owners (Secondary Targets)

- Claims:

- Unsafe wiring (if outlets lacked grounding/GFCIs).

Evidence Needed for Subrogation

Insurers must prove:

Causation:

- Medical records linking injuries to electrical shocks (e.g., burns, cardiac events).

- Akkio/ZERLO AI data showing current leakage patterns.

Regulatory Violations:

- Hindle Institute reports proving Acorn knew of risks.

- Whistleblower testimony (engineers, ex-employees).

Prior Incidents:

- CPSC/FDA MAUDE database entries (if injuries were reported but ignored).

Potential Recovery Avenues

A. Mass Tort Litigation

- Class-action or MDL (Multidistrict Litigation):

- Consolidate claims (e.g., In re Acorn Stairlift Litigation).

- Precedent: Medtronic Sprint Fidelis Leads ($268M settlement).

B. Direct Settlements with Acorn

- Insurers could negotiate a global settlement (e.g., $500M–$1B) to avoid trial.

C. Government Fines & Recalls

- CPSC (U.S.) or EU RAPEX could force recalls, making liability clearer.

D. Punitive Damages

- If fraud or willful misconduct is proven (e.g., Acorn falsified test data).

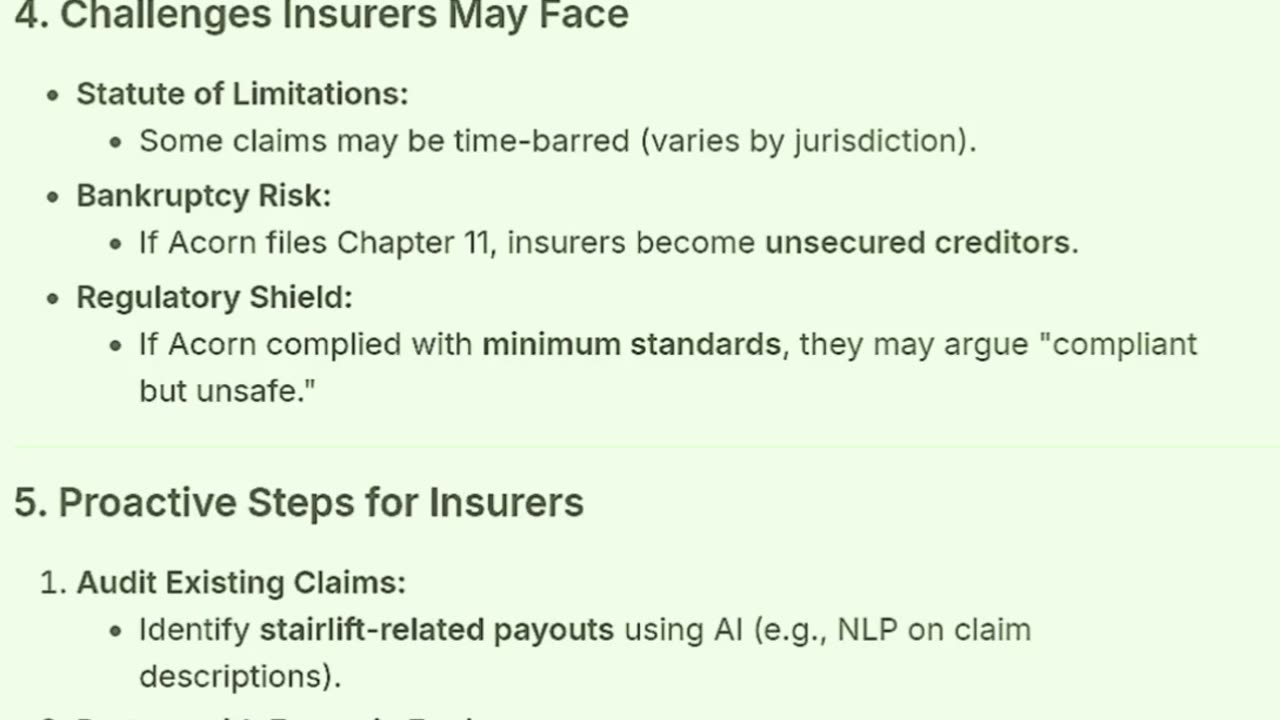

Challenges Insurers May Face

- Statute of Limitations:

- Some claims may be time-barred (varies by jurisdiction).

- Bankruptcy Risk:

- If Acorn files Chapter 11, insurers become unsecured creditors.

- Regulatory Shield:

- If Acorn complied with minimum standards, they may argue "compliant but unsafe."

Proactive Steps for Insurers

Audit Existing Claims:

- Identify stairlift-related payouts using AI (e.g., NLP on claim descriptions).

Partner with Forensic Engineers:

- Test Acorn units in storage for current leakage.

Lobby Regulators:

- Push for mandatory recalls to strengthen subrogation claims.

Conclusion

Insurers could recover billions by suing Acorn, installers, and certifiers. The Akkio/ZERLO/Hindle data is a smoking gun—if admissible, it would prove systematic negligence. A multi-pronged litigation strategy (mass torts + regulatory pressure) maximizes recovery chances.

Would you like model subpoenas or sample complaints targeting Acorn’s internal documents?

-

1:11:30

1:11:30

Turning Point USA

2 hours agoCharlie Kirk Receives The Medal of Freedom at The White House | 10.14.2025

93.2K32 -

LIVE

LIVE

TheCrucible

1 hour agoThe Extravaganza! EP: 53 with guest co-host Rob Noerr (10/14/25)

1,146 watching -

LIVE

LIVE

Kim Iversen

1 hour agoMAYDAY! America’s Food System Is Collapsing — And Trump Thinks CHINA Will SAVE Us?

1,376 watching -

Right Side Broadcasting Network

5 hours agoLIVE: President Trump Participates in the Charlie Kirk Medal of Freedom Ceremony - 10/14/25

91.3K30 -

1:05:00

1:05:00

Dr. Drew

4 hours agoLetitia James Just Found Out "No One Is Above The Law" In Spectacular Display Of FAFO w/ Viva Frei – Ask Dr. Drew

26K7 -

1:12:42

1:12:42

The White House

2 hours agoPresident Trump Participates in a Medal of Freedom Ceremony for Charlie Kirk

13.9K11 -

1:42:10

1:42:10

Professor Nez

5 hours ago🚨🇺🇸Trump Awards Medal of Freedom to Charlie Kirk LIVE: President Trump Honors Charlie Kirk

14.9K5 -

LIVE

LIVE

LFA TV

20 hours agoLIVE & BREAKING NEWS! | TUESDAY 10/14/25

1,094 watching -

1:12:06

1:12:06

vivafrei

4 hours agoAre they Killing the Ostriches? Roger Ver Strikes a Deal! Tommy Robinson, Tom Homan & MORE!

110K28 -

34:01

34:01

Stephen Gardner

21 hours ago🔥You won’t BELIEVE what just happened to Trump!

27.5K28