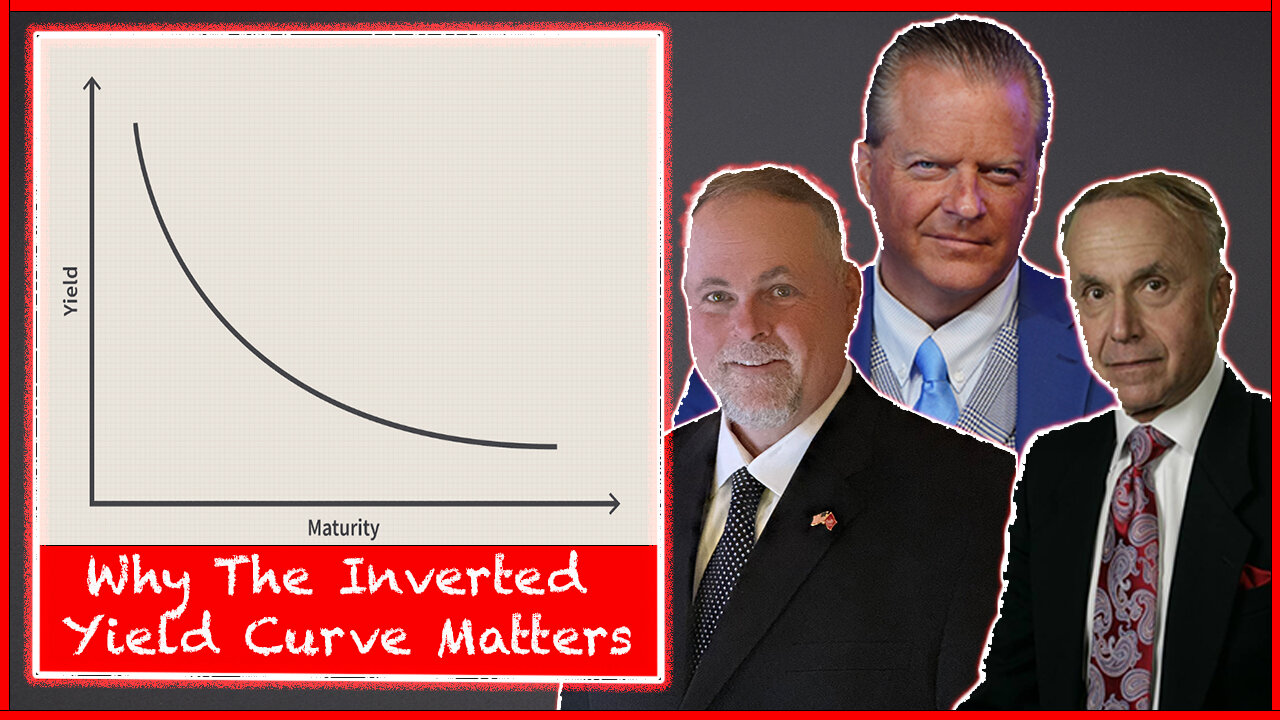

Why The Inverted Yield Curve Matters and What it Means For Your Finances

Loading comments...

-

LIVE

LIVE

WorldviewTube

21 days agoWorldview Tube Live!

26 watching -

LIVE

LIVE

Redacted News

46 minutes agoTrump Rolling Out $2,000 STIMULUS Checks in 2025 as the U.S. Economy Flashes RED | Redacted News

13,992 watching -

LIVE

LIVE

vivafrei

3 hours agoOstrich Farm Update w/ Chris Dacey; Jan. 6 Pipe Bomber IDENTIFIED? w/Kyle Serraphin & MORE!

4,709 watching -

2:00:02

2:00:02

The Quartering

2 hours agoDemocrat Civil War After Collapse, Viral Wedding Ring Insanity, New Trump Pardons & Huge Trans Ban

113K24 -

LIVE

LIVE

Dr Disrespect

5 hours ago🔴LIVE - DR DISRESPECT - ARC RAIDERS - THE VENATOR SLAYER

1,683 watching -

DVR

DVR

Stephen Gardner

52 minutes ago🔥Adam Schiff OBLITERATED by Trump's NEW EVIDENCE!

6 -

1:16:02

1:16:02

Russell Brand

2 hours agoTHE TRUST CRISIS — Vaccines, Obama’s Image & Gates’ Agenda - SF648

34.2K7 -

LIVE

LIVE

Film Threat

18 hours agoVERSUS: SYDNEY SWEENEY VS. PREDATOR: BADLANDS | Film Threat Versus

152 watching -

1:13:22

1:13:22

DeVory Darkins

4 hours agoDemocrats SUFFER DEFEAT as party turns on Chuck Schumer

105K30 -

1:06:18

1:06:18

Timcast

4 hours agoGangs Order KILL ON SIGHT DHS Agents, Chicago Is A WAR ZONE

233K167