NY Applies Policy as Written

Construction and Development Activities Exclusion Unambiguous

In Grenadier Realty Corp., et al. v. RLI Insurance Company, appellant, et al., No. 2020-06795, Index No. 502159/18, 2023 NY Slip Op 03910, Supreme Court of New York, Second Department (July 26, 2023) a New York Supreme Court (trial court) order requiring RLI Insurance Company to defend its insured was appealed by RLI.

The trial court order granted the plaintiffs' motion for summary judgment declaring that certain losses were covered under a general liability insurance policy issued by RLI Insurance Company and that RLI Insurance Company was obligated to indemnify the plaintiffs in connection with the underlying action entitled Gargiso v Howland Hook Housing Co., Inc.

UNDERLYING ACTION AND INSURANCE CLAIM

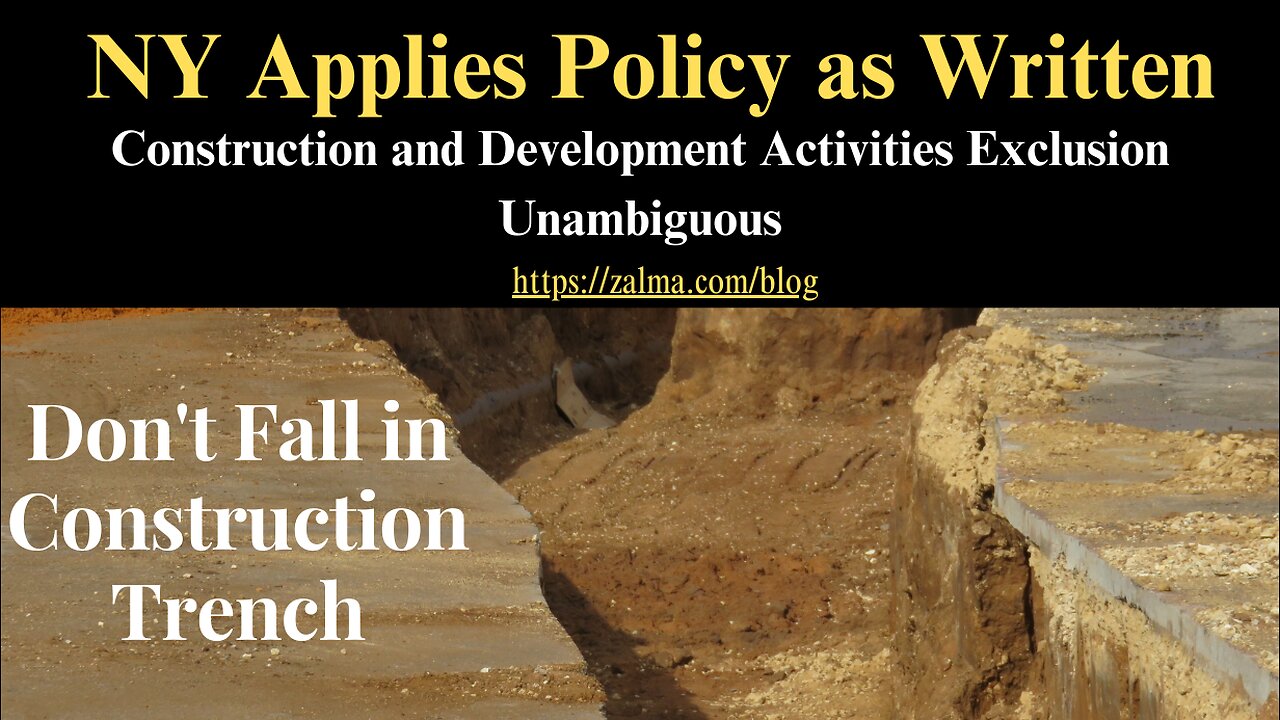

In July 2012, Michael Gargiso allegedly was injured when he stepped in a trench which was dug as part of a construction project that had been left unfinished. Gargiso sued the property owner, Howland Hook Housing Co., and the property manager, Grenadier Realty Corp.

Grenadier, which had purchased a general liability insurance policy from the defendant RLI effective March 1, 2012 (the subject policy), sought to obtain coverage from RLI. RLI denied coverage based upon an exclusion in an endorsement to the subject policy for "bodily injury" arising out of "Construction and Development Activities."

Thereafter, the plaintiffs sued RLI to recover damages for breach of the subject policy and for a judgment declaring that RLI is obligated to provide coverage under the policy and to indemnify the plaintiffs in connection with the underlying action.

The plaintiffs moved for summary judgment on their causes of action against RLI alleging breach of contract and for a judgment declaring that RLI was obligated to provide insurance coverage to them under the policy and to indemnify them. RLI cross-moved for summary judgment dismissing the complaint insofar as asserted against it and for a judgment declaring that it has no duty to indemnify the plaintiffs.

ANALYSIS

In determining a dispute over insurance coverage, the appellate court first looks to the language of the policy. As with any contract, unambiguous provisions of an insurance contract must be given their plain and ordinary meaning. The insurer has the burden of proving the applicability of an exclusion. If the language is doubtful or uncertain in its meaning, any ambiguity will be construed in favor of the insured and against the insurer. However, the plain meaning of a policy's language may not be disregarded to find an ambiguity where none exists.

The RLI policy provided coverage for, among other things, damages because of "bodily injury." The policy, however, includes a construction and development exclusion, which, as is relevant, excludes from coverage "bodily injury" resulting from "Construction and Development Activities." Gargiso was injured when he stepped into a trench which had been dug as part of the construction activities in a parking lot on the property. RLI demonstrated that the construction and development exclusion unambiguously excluded from coverage bodily injury arising out of such construction and development activities. Therefore, RLI established that it did not have a duty to indemnify the plaintiffs in connection with the underlying action.

CONCLUSION

The Supreme Court should have denied plaintiffs' motion for summary judgment and should have granted RLI's cross-motion for summary judgment dismissing the complaint insofar as asserted against it and for a judgment declaring that RLI is not obligated to indemnify the plaintiffs in connection with the subject underlying action

The appellate court reversed, with costs. RLI Insurance Company's cross-motion for summary judgment dismissing the complaint insofar as asserted against it and for a judgment declaring that it has no duty to indemnify the plaintiffs was granted.

The appellate court then remitted the matter to the Supreme Court, Kings County, for the entry of a judgment, inter alia, declaring that RLI is not obligated to indemnify the plaintiffs in the underlying action entitled Gargiso v Howland Hook Housing Co., Inc.

ZALMA OPINION

Clear and unambiguous exclusions must, as did the appellate court, be affirmed and enforced. When you fall into a construction trench, as did Mr. Gargiso, you are the victim of construction activities that were clearly and unambiguously excluded.

(c) 2023 Barry Zalma & ClaimSchool, Inc.

Please tell your friends and colleagues about this blog and the videos and let them subscribe to the blog and the videos.

Subscribe and receive videos limited to subscribers of Excellence in Claims Handling at locals.com https://zalmaoninsurance.locals.com/subscribe.

Consider subscribing to my publications at substack at https://barryzalma.substack.com/publish/post/107007808

Go to Newsbreak.com https://www.newsbreak.com/@c/1653419?s=01

Follow me on LinkedIn: www.linkedin.com/comm/mynetwork/discovery-see-all?usecase=PEOPLE_FOLLOWS&followMember=barry-zalma-esq-cfe-a6b5257

Daily articles are published at https://zalma.substack.com. Go to the podcast Zalma On Insurance at https://podcasters.spotify.com/pod/show/barry-zalma/support; Follow Mr. Zalma on Twitter at https://twitter.com/bzalma; Go to Barry Zalma videos at Rumble.com at https://rumble.com/c/c-262921; Go to Barry Zalma on YouTube- https://www.youtube.com/channel/UCysiZklEtxZsSF9DfC0Expg; Go to the Insurance Claims Library – https://zalma.com/blog/insurance-claims-library\

-

13:02

13:02

Barry Zalma, Inc. on Insurance Law

1 year agoMurder Pays

4011 -

LIVE

LIVE

Major League Fishing

3 days agoLIVE! - Bass Pro Tour: Heavy Hitters - Day 1

1,427 watching -

8:00:02

8:00:02

SpartakusLIVE

10 hours agoWZ Solos || #1 Challenge MASTER brings you Saturday SPARTOONS

55.1K1 -

9:05:51

9:05:51

Spartan (Pro Halo esports Player)

12 hours agoNo Scrims today so Ranked for a bit then SWTOR

38.4K -

58:42

58:42

Sarah Westall

12 hours ago500 Vaccine Schedule, WHO & UN Deception, Cyborg Depopulation Agenda w/ Dr. Rima Laibow

76K22 -

9:15

9:15

The Art of Improvement

2 days agoThe Power of Micro-Goals

32.7K3 -

16:16

16:16

megimu32

19 hours agoKerplunk Unboxing: Loud, Chaotic & Definitely a Sibling Trap

22.1K17 -

22:55

22:55

marcushouse

20 hours ago $1.22 earnedStarship’s Flight Plan Just Took an Unexpected Turn!

18.7K8 -

1:29

1:29

Memology 101

1 day ago $1.66 earnedShe just SNITCHED on her ENTIRE party…😂😂😂

15.1K16 -

4:53:29

4:53:29

IcyFPS

10 hours agoDOOM x WARZONE | Chapters 9-14 | LETS GO!! | Direct RTMP |

10.4K1