What is the Hume-Cantillon Effect?

At this point you may have realized that inflation works against you to make you poorer but did you know inflation works to the advantage of certain groups of people? In fact, the negative effects of inflation are not evenly distributed. Some people are positioned to profit from inflation at the expense of others. For most people, inflation will erode their standard of living.

The Cantillon effect refers to the uneven distribution of the burden of inflation, and surprisingly the benefits for some people. It states that when money is printed out of thin air, as the United States government is prone to do, the initial recipients of this new money, usually the banks and the government, benefit the most because the price levels in the economy has not fully adjusted to the influx of new dollars flooding it. Who is burdened the most by an increased supply of money I like to refer as money printing? It is working class people like you and me who receive the new money last. We face higher prices for goods and services before our incomes have increased accordingly, adjusting to inflation. If you are like most people, your wages and income will probably not fully increase at the rate of inflation even over a longer period of time, and in this way, you suffer two-fold. First, your money has reduced purchasing power as the price level in the economy rises. Second, your earnings never fully catch up to the increased price levels leaving you poorer overall.

For this reason, it is not enough to slow down the rate of inflation. Your wages must catch up to the increased price level. Because a lot of people’s incomes do not catch up, they continue to suffer the effects of inflation long after it has cooled.

I do not think it is much of a stress to say that, for many people, we are poorer and have a low standard of living post covid due to how expensive everything has gotten. Just look at the housing market. According to Redfin, American homebuyers need to earn about $115,000 a year in order to be able to afford the cost of the typical U.S. home. As of 2023, the average salary in the USA, according to Forbes, is $59,428

It is for these reasons, and many others, that I state that inflation hurts the most vulnerable parts of society the most while benefiting the government and banking system the most.

We can combine the Cantillon effect with the work of 18th century Scottish philosopher David Hume who proposed that an increase in the money supply would lead to a proportional increase in price, rather than magically creating economy activity as some people naively believe. In life and economics, a decision for one thing is often a decision against another thing. The benefits the government derives from money printing comes at the cost of its citizens and people who invested in government debt and other low interest-bearing investment instruments.

Together, the Hume-Cantillon effect states that the price level will increase to meet the increased supply of money the government is printing, and then the benefits of this money printing will flow to the government at the expense of individual citizens and working-class people.

Inflation is a serious issue that makes us all poorer. While it may take some economic pain to bring inflation down, it is well worth it to preserve our purchasing power and our standard of living as individuals and as a society. No one likes to lose their job or hear about layoffs. However, the out-of-control inflation that the world is just now coming to terms with has led to many people being unable to heat their homes, put food on their table, and cloth their children.

180

views

1

comment

Can a company cut your pay?

Can a company cut your pay?

You may be wondering if it is legal for your employer to reduce your pay or your hours. I think the answer to this question will surprise you.

Did you know that in the US you can be legally fired for any reason at any time? In fact, the employer does not even need a reason to fire you.

In most of the United States, employment is at-will which means the employer can terminate any employee at any time and for any reason.

Companies may cut pay or hours for a variety of reasons. Perhaps they are trying to avoid layoffs. However, they may actively be trying to get employees to quit so they do not have to pay unemployment benefits.

While you think your employment contract protects you from your employer decreasing your pay, the truth is that you most likely did not even sign a contract. Rather, you probably just signed an offer letter. Usually, when a company offers a salary and benefits, this constitutes an offer rather than a contract. Companies often try to avoid making binding promises to employees. While they may hire you at a certain salary or wage, there is no commitment to keep you at that rate. However, the law does require an employer to inform you if they are going to cut your pay. Workers with collective bargaining agreements are shielded from pay cuts, but you would likely need to be involved in a labor union for this to pertain to you. Another way for you to be shielded from pay cuts is if you have a written employment contract, but this is unlikely unless you are highly compensated or work in management, perhaps as an executive.

Another alternative for a company looking to reduce an employees pay is to just fire and rehire them at a lower rate.

The only real rule when it comes to compensation is that they cannot retroactively reduce your pay. What you earned in the past, is yours to keep but going forward, your pay can be cut.

In some states, if your compensation is reduced and you quit, this may constitute ground for receiving employment benefits. However, you should do your research. Every state is different. Some states make it very difficult to collect unemployment benefits. Also, as I have experienced first hand, employers may lie to the unemployment office or misrepresent material facts to try and invalidate your unemployment benefit claim.

Unfortunately, if your company reduces your pay, you do not have much recourse. Most of the time, when a company is doing something you disagree with, your only options are to either deal with it or to quit. If you are unhappy with how you are treated at work, I would suggest you update your resume and start applying for other jobs. Many people stay at low paying job or toxic workplaces too long when they could go out into the job market and find something much better. I think you will find that there are many opportunities out there just waiting for you. Try and be optimistic, and why not apply to a few jobs this week and see where those applications lead you?

Tags:

SalaryCut, PayReduction, EmployeeRights, WageReduction, Compensation, EmploymentLaw, PayCutExplanation, WorkplaceRights, LaborLaws, FinancialAdvice, CompanyPolicy, JobSecurity, HRGuidance, EmploymentContracts, MoneyMatters, IncomeChanges, CorporateDecisions, LegalRights, EconomicChanges, WorkplaceChallenges, personal finance ,personal finance tips ,personal finance 101 ,personal finance basics ,finance ,personal finance management ,personal finance books ,personal finances ,personal finance advice ,personal finance lessons ,personal finance audiobook ,personal finance principles ,personal finance for beginners ,learn personal finance for beginners ,finances ,top personal finance ,personal finance club ,personal finance rules ,learn personal finance ,how to personal finance

Works Cited:

https://swartz-legal.com/can-an-employer-legally-reduce-your-pay/

249

views

Beneficiary forms can override your will

Beneficiary forms can override your will

If you assume your will is your final word on what happens to your assets when you die, they may end up going to an ex-spouse or caught up in a lengthy court battle. This issue is becoming more pronounced as Americans juggle multiple retirement, insurance, and bank accounts.

When you sign up for a 401(k) plan at work, you will be asked to name beneficiaries. These are the people that will inherit your account if you pass away. Usually you will name a primary beneficiary who is your first choice to receive the assets, but you also may name contingent beneficiaries who are essentially backup if the primary beneficiary dies before you do. You should take this very seriously or else the 401(k) will end up in probate court which can be expensive and slow. Even if you do have a will, naming 401(k) beneficiaries makes the inheritance process much quicker and less expensive.

You could write volumes about nightmare beneficiary situations. A spouse for less than a year can end up with the entire retirement plan instead of the participant’s underage child. People will put former friends from decades ago on beneficiary forms and forget about both the forms and the friends.

Plans often have a hierarchy that omits partners, friends, and other relatives in favor of spouses, children, parents, and siblings.

There are documents that can override wills including beneficiary forms for retirement accounts, life insurance, and some bank and brokerage accounts.

401K

Married spouses are automatically entitled to the 401k money of their spouse unless they formally waive it. This waiver must be notarized.

IRA

Most IRAs allow you to name someone other than your spouse as your beneficiary without getting a waiver from your spouse. However, if you live in a community-property state like California or Texas, you will need a waiver.

Insurance Accounts

If you obtained insurance through your workplace, then the employer plan documents dictate the payout terms. If you purchased the insurance independently of your workplace, the insurance company rules will determine where they money goes.

Tips:

I have a few tips for you.

Take beneficiary designations seriously. Include details about your beneficiaries including date of birth and Social Security number.

Update your beneficiary forms after life events like marriage, divorce, or the birth of children. While some states have laws that automatically revoke the designation upon divorce, some do not.

Copies of beneficiary forms should be kept with your other estate planning documents to avoid institutions like banks losing the paperwork which results in costly court battles.

Send duplicate beneficiary forms to the bank, brokerage house, or insurance company and ask for one back with a stamp showing it was received.

Check your online accounts to make sure any changes are reflected online.

Make sure your beneficiaries are aware of, and can easily find, your beneficiary designations. A sizeable amount of unclaimed retirement money is out there.

Many new hires will put down their mother as their beneficiary when they take their first job. Over time, mothers pass away, and this could lead to a potentially nasty court battle should the plan recipient pass away as well.

Works Cited:

https://www.wsj.com/personal-finance/estate-planning-will-money-family-heirs-8f2eb6e8?mod=hp_lead_pos10

https://www.investopedia.com/what-are-401k-beneficiary-rules-5496575

Tags:

beneficiary, beneficiary forms, ira beneficiary, 401k beneficiary, beneficiary form, postal beneficiary forms, ira beneficiary form, problems with beneficiary forms, beneficiary designations, federal employee beneficiary forms, update beneficiary form, beneficiary form for ira, ira beneficiary form mistakes, trust as beneficiary for ira, 401(k) beneficiary, name trust as beneficiary for ira, what is a beneficiary, primary beneficiary, contingent beneficiary, probate court, probate, what is probate court, probate court explained, what is probate, probate real estate, wayne county probate court, probate court 101, probate court faq, probate courts, probate court help, probate court cases, probate court no will, probate court hearing, probate court process, how probate court works, maryland probate court, probate court with a will, what probate court means, probate court definition, when is probate court used

239

views

Return to office policies are not working

Return to office policies are not working

Return to office rates are at there highest level since the onset of the pandemic. Despite this, office attendance is barely half of what it was in 2019. Company’s measures to get workers into the office have largely proven ineffective.

This fall, there is the potential for a resurgence of COVID cases doubled with a weakening economy that could depress office attendance. While I think the threat of a fall COVID wave may be overstated, I have mixed feelings about the general state of the US economy and its trajectory. I don’t think anyone truly understands what is occurring in the USA economy. There are a great number of mixed signals and Americans are somewhat pessimistic about the economy.

Blue chip companies are vowing to fill their workspaces as they commit to get tougher on employees that do not show up to the office. Meta has threatened disciplinary action. Despite these tougher policies, the return to office rate has not budged much.

Most employees go into the office during the middle of the week, with most people being out Monday and Friday. In Chicago, we have seen office attendance rates over 66% on certain days, but less than 30% on Friday. This range is about 25% to 65% in New York City. Kastle Systems puts the average rate at about 50.4% across the ten US cities it tracks.

The average national office vacancy rate rose to 19.2% last quarter. This is just below the historical record of 19.3% in 1991 according to Moody’s Analytics.

Part of the reason for low office attendance could be lax enforcement.

We are seeing a homelessness crisis across much of the country concentrated in urban centers. 90% of the members of the Seattle Metropolitan Chamber of Commerce said that the city could not recover until homelessness and crime was addressed. Crime and homelessness is reducing office attendance.

Spending cuts to government services and transportation are also weighing on office attendance. It is common to have long periods of time between transit trains in Chicago. Long wait times for trains and buses are occurring through many large cities. A long commute makes the work day that much longer and more of a pain.

Business will have more leverage to enforce office mandates if the economy weakens. Many people, including myself, have been amazed at how resilient and seemingly bulletproof the economy has been. However, I just did a video on the increasing amount of spending and credit card debt consumers are piling on. I have concerns that the average American is overextending themselves.

The flip side of a weak economy is that it reduces demand for companies to rent office space.

City and business leaders are increasingly turning to the federal government for help. There are lobbying efforts occurring to incentivize businesses to rent office space in cities. However, the chances of legislation is low.

On a personal note, I greatly enjoy working from home and I know this view is shared by a great number of people. I’m sorry that all this investment into office space is not working out but it is time to stop socializing business losses. There should be no government bailout of commercial property. If you took out the debt, you should pay it back.

Works Cited:

https://www.wsj.com/real-estate/commercial/tougher-return-to-office-policies-are-no-remedy-for-half-empty-buildings-57f41886?mod=hp_lead_pos1

Tags:

remote work, work from home, remote jobs, remote work from home jobs, work from home jobs 2023, remote work 2023, remote jobs 2023, end of remote work, is remote work over, work from home jobs, remote work from home, is remote work here to stay, work at home, remote work from home jobs no experience, remote work nyc, remote workers, remote work jobs, remote work tips, remote work ends, remote work setup, war on remote work, work return to office, return to work, back to office, office, return to office 2023, return to office quit, meta return to office, return to office order, return to office debate, return to office amazon, amazon return to office, zoom ceo return to office, return to office mandate, return to in person office, goldman sachs return to office, return to office post pandemic, lyft employees return to office, return to office after working from home, office rent

148

views

Americans are spending like there is no tomorrow

Americans are spending like there is no tomorrow

Americans are spending big despite facing mostly depleted pandemic savings, a cooling labor market, and high interest rates and inflation.

The primary driver of United States economic growth is household spending. This remains robust as Americans spent 5.8% more than last August. This rate well outstrips the inflation rate of 4%.

Households that made at least one large purchase in the last four months increased from 57% last year to 64% this year which is the highest rate since August 2015 according to the New York Federal Reserve Bank.

The experience economy is booming. Delta Air Lines had record revenue in the second quarter. Ticketmaster sold over 295 million event tickets in the first half of 2023 which represents an 18% YoY. Ally Bank allows customers to create different savings buckets for different goals. There are over 1.5x as many buckets for experience orientated things like travel and fun in contrast to longer term planning.

Americans currently have a record amount of credit card debt. It totals over $1 trillion. The states with the highest credit debt are Connecticut, New York, and New Jersey. All three have average credit card debt of over $9,000.

While it is common for consumers to put short-term needs and goals above long term goals, the current circumstances are different in a number of ways. Americans are spending on once in a lifetime experiences due in part because of fears they may not have the opportunity to experience them later. People fear regretting not doing things like taking an overseas vacation or splurging on a big ticket purchase.

An article in the WSJ mentions one may who spent $1,600 on a Taylor Swift Eras Tour ticket and then about $3,500 on a bachelor party. A family of three spent $10,000 on a 10 night vacation in Hawaii at a 4-star resort. Another man lowered his retirement contribution so he could spend $7,000 on an Alaskan cruise. Then there is the story of a family that sold their home to travel the country with their two children.

Many consumers have given up the idea of ever owning a house. I’ve seen a lot of people discussing the idea of never being able to own a house, but I also think the idea of never being able to retire will also gain traction in the mind of many consumers in the years that come as people face economic uncertainty and high inflation and interest rates. Despite what politicians say, consumers remain frustrated about inflation. While it is true that inflation has fallen sharply in the past year, many Americans are deeply unhappy about the economy and often cite inflation as the primary reason. Prices for many things are well above their pre-pandemic price levels. The fact is that even though the inflation rate has come down, prices remain elevated and that weighs against consumer confidence.

Works Cited:

https://www.wsj.com/economy/consumers/americans-are-still-spending-like-theres-no-tomorrow-6a1d307?mod=hp_lead_pos1

https://www.wsj.com/economy/consumers/why-consumers-are-mad-about-inflation-even-though-it-has-fallen-ce39ca40?mod=hp_major_pos1#cxrecs_s

https://www.lendingtree.com/credit-cards/credit-card-debt-statistics/

Tags:

consumer spending, consumer, consumer spending report, consumer spending habits, consumer spending figures, spending, consumers, consumer services, consumer goods, consumer confidence, consumer sentiment figures, consumption, personal finance, econ, credit card debt, credit card, credit cards, debt, how to pay off credit card debt fast, credit debt, us credit card debt, us credit card debt 2023, us credit card debt crisis, economy, u.s. economy, economy explained, us economy, biden economy, economy news, economic, united states economy, economic debt, economic news, economic divide, the economy of united states, economic cool down, biden administration economy, economic indicator

172

views

1

comment

The Pepsi pivot from health foods back to chips and soda

The Pepsi pivot from health foods back to chips and soda

While consumers will tell you they want to eat healthier, what they actually want to do is eat potato chips.

Pepsi has been gradually making snacks and drinks more healthy by lowering sodium, saturated fat, and sugar in its products, all without consumers noticing.

At Pepsi, there is a sensory panel composed of 10 professional food tasters that meet several times a week to sample PepsiCo’s latest attempts at healthier junk food.

Pepsi has been trying to reduce the sodium content of Lay’s potato chips without consumers noticing. Approaches to this include new salt crystals, salt substitutes, different potato varieties, and different combinations of herbs and spices. However, similar efforts to cut sodium at Campbells soup ended up with the company reversing their efforts. While I think consumers may note the calorie content of a bag of Doritos, I’m not sure they are looking at things like sodium or fat content.

The previous CEO, Indra Nooyi, tried to shift the snacks and soda portfolio toward healthier offerings like Naked Juice, Sabra hummus, and KeVita kombucha. Product launches that had little success included TrueNorth nuts, midcalorie Pepsi Next and Müller Quaker yogurt.

The current CEO, Laguarta, has increased the marketing budget, built new manufacturing for salty snacks, expanded the energy drink business, and increase R&D into new snack variations like mini Doritos and Cheetos Mac and Cheese.

PepsiCo’s annual revenue rose by 34% between 2018 and 2022, to $86 billion, though in some categories its market share has slipped.

Pepsi was doing zero based budgeting which required managers to justify their expenses annually. The result was that the company was underinvesting in North American snacks business.

When Pepsi reported earnings in July, the results showed strong growth in both sales and profits despite price increases and increased advertising expenses. Consumers seem willing to pay up more for snacks and sodas. Revenue increased more than 10% in the last quarter. North American snacks increased 14%. The North American beverage unit increased 10%.

Works Cited:

https://www.wsj.com/articles/pepsi-pep-q2-earnings-report-2023-2f9d2b0

https://www.wsj.com/articles/pepsi-lays-doritos-soda-sugar-fat-salt-health-62047e07?mod=saved_content

https://www.wsj.com/articles/twinkies-doritos-trix-snacks-get-tiny-80f1fb1d?mod=article_inline

Tags:

stock market, pepsi stock, pep stock, stocks, pepsi stock analysis, pepsico stock, pepsi, pepsi stock 2023, coke vs pepsi stock, pepsi stock dividend, stock, coca cola vs pepsi stock, pepsi stock analysis 2023, ko stock, pep stock analysis, ko vs pepsi stock, stock analysis, pepsi stock valuation, coke stock analysis, coke stock, finance stock, ko stock analysis, stock market news, stocks to buy now, dividend stocks, fundamental stock analysis

113

views

Student Loan Repayment: What is Biden’s SAVE plan?

Student Loan Repayment: What is Biden’s SAVE plan?

The Saving on a Valuable Education plan, or SAVE, is a new income-driven repayment plan in which monthly loan payments take into account family size and discretionary income. More than 4 million people have enrolled so far.

Many income driven repayment plans have resulted in borrowers paying more interest and for longer.

SAVE calculates discretionary income above 225% of the federal poverty level versus previous regulations at 150%. Therefore, more income is protected.

There is also a 12 month on ramp period when missed payments will not impact your credit score or result in a loan default.

If your ultimate goal is loan forgiveness, do not take the on-ramp because this will not count towards your forgiveness threshold.

Loan balances will not grow due to unpaid interest with SAVE. Borrowers will not be charged any additional interest than what their payment covers.

SAVE will accelerate the path to loan forgiveness as long as borrowers make their payments on time. After 10 years, the remaining debt balance will be wiped out. For those with loan balances of $12,000 and less. Otherwise, the forgiveness period will increase by one year for everything additional $1,000 borrowed. So someone with a loan balance of $13,000 will take 11 years, $14,000 will take 12 years, and $15,000 will take 13 years to reach loan forgiveness. However, the maximum number of years in repayment is capped at 20 to 25 years depending on if it is for an undergraduate or graduate degree.

If you are enrolled in a REPAYE plan, a previous type of IDR, you will automatically be rolled over into the SAVE plan.

Works Cited:

https://www.wsj.com/personal-finance/student-loan-save-repayment-plan-95b256a7?mod=lead_feature_below_a_pos1

Tags:

save plan, repaye plan, plan, save repayment plan, save student loan plan, simple plan, debt relief plan, bidens save plan, repayment plans, simple plan save you, save you simple plan, simple plan - save you, idr repayment plans, save plan student loans, income-driven plans, income driven plans (idr), atlantic records simple plan, income driven repayment plan, revised pay-as-you-earn plan, student loan repayment plans, save student loan repayment plan

73

views

7 reasons that timeshares are a terrible investment

7 reasons that timeshares are a terrible investment

Let me begin by saying that timeshares are technically not even investments because investments appreciate in value and/ or generate income. A timeshare is unlikely to do either. If you don’t believe me, consider how many used timeshares are on the market and how much money timeshare companies spend on marketing and just how aggressive the salespeople are. The very nature of the sales process should be a hint about the dark reality of timeshares.

It is interesting to note that almost every major hotel chain is involved in the timeshare industry. The Big Three timeshare companies are Wyndham, Hilton Grand Vacations, and Marriott Vacations Worldwide. Wyndham is the largest corporation involved in timeshares with half a million owners across 100 resorts in North America.

Timeshares are based on the concept of fractional ownership in a property. They generally operate under two schemes:

1) Deeded where you purchase an ownership interest in the property.

2) Non-Deeded whereby you lease the right to use the property for a specific amount of time each year for a preset number of years.

You also can purchase for a fixed week each year, or you can purchase a floating week which can be used during a predetermined period of time.

Here are my top seven reasons that timeshares are an awful investment:

High Upfront Cost: Timeshares typically require a significant amount of upfront purchase price. Worse, if you decide to finance your timeshare purchase through the timeshare company, you will face a steep interest rate.

Ongoing Costs: As if the high upfront cost was not bad enough, you are expected to contribute on an ongoing basis. Timeshare owners are responsible for annual maintenance fees, property taxes, and other expenses that add up fast and may be unpredictable. The qualities of timeshare companies and properties varies widely. Despite contributing what you may deem a significant amount in ongoing costs, maintenance and upkeep may not meet your expectations. One-time assessments can be levied for things like a new roof or a new sewage line.

Limited Appreciation: Traditional real estate tends to enjoy price appreciation but this is not the case with timeshares. In fact, it’s the contrary because many timeshares lose value over time. You will most likely not be able to sell your timeshare for the price you purchased it at.

Lack of Flexibility: You are essentially locked into a specific location, time period, and type of accommodation which will be increasingly problematic as your preferences and life changes over time.

Difficulty Reselling: Selling a timeshare is challenging to put it mildly. The resale market is oversaturated with other people trying to unload their timeshares. If you do somehow get lucky to be able to sell your timeshare, it will be at a price less than your initial investment.

Complex exchange programs: While some timeshare companies do offer exchange programs that allow you to swap your timeshare for a different location or time of the year, these programs are purposely complex and you may not find the results satisfactory. Everyone wants to travel to the same places in the same weeks you do. For example, Hawaii in the summer will be in demand but no one will want to go to Phoenix or Las Vegas in July and August.

Alternatives: You may just want to consider renting a vacation property on Airbnb or VRBO as they are more flexile and cost effective than a timeshare.

Conclusion: Timeshares are rarely a sound financial investment due to their high upfront costs, significant ongoing costs, limited flexibility, and lack of appreciation. You are almost always better off just staying at a hotel or Airbnb. Be extremely careful before entering into a contract for a timeshare and consider your alternatives extensively. If you feel absolutely compelled to purchase a timeshare, make sure it is a used one, not a new one. Just google “timeshare resale.”

Works Cited:

https://www.investopedia.com/articles/pf/08/timeshare.asp

Tags:

timeshare, timeshares, timeshare presentation, timeshare scams, timeshare sales, wyndham timeshare, what is a timeshare, timeshare sales pitch, timeshare cancellation, timeshare vacation, should i buy a timeshare, timeshare scam, timeshare exit, timeshares explained, are timeshares worth it, buying a timeshare, timeshare meeting, marriott timeshare, timeshare technics, timeshare strategies, timeshare questionaire, are timeshares a scam, how to get rid of a timeshare

72

views

Top 10 Hottest Cities according to Realtor.com

Top 10 Hottest Cities according to Realtor.com

Mortgage rates have remained between 6 to 7% which has put a lot of pressure on house affordability because the monthly mortgage payments has soared. Prospective homeowners are flocking to both affordable markets and markets that are close to large cities.

The most buyer demand is occurring in affordable Midwest markets and well-located Northeast markets that offer both convenience and value. These homes tend to be larger than the US average. Despite how hot these markets are, home prices are at or below the US median.

I think the story here is that affordable housing markets are becoming more popular as prospective homeowners are pushed out of unaffordable areas. Another possible trend that is occurring is that high earning households are relocating to the suburbs of large cities for a better quality of life which corresponds to house affordability.

10) Ballwin Missouri: Ballwin is approximately 20 miles west of downtown St. Louis and has an economy that is a mix of retail, healthcare, and other businesses. Residents can commute to St. Louis for both work and education.

9) Pittsford, New York: You will find Pittsford in the Finger Lake region of New York state just south of Rochester. It has a good school system. There are a lot of outdoor recreational opportunities. Residents may opt to work in Rochester.

8) Norwalk, Connecticut: Norwalk is about 40 miles northwest of NYC. Employment opportunities include finance, healthcare, technology, and manufacturing. There are highway and rail connection to the city. This could be a good choice for someone that wants to commute to NYC.

7) Trenton, Michigan: Situated 20 miles southwest of downtown Detroit, along the Detroit River, there are a lot of employment and recreational opportunities. There are several large manufacturing operations. The median household income is $78,000 versus the US average of $70,000. This could be a good city for working class families.

6) Highland, Indiana is about 27 miles southeast of downtown Chicago. One of my teachers used to joke that northwest Indiana is just a suburb of Chicago. This would be a good choice for someone that wants Indiana state government over Illinois so they can enjoy less taxes. You can take the highway to Chicago to commute for work or play.

5) Nazareth, Pennsylvania: Nazareth is 65 miles west of NYC and 60 miles north of Philadelphia. This might be a good city if you can do remote work and only have to show up to the office in NYC or Philadelphia a few times a month. This is going to be a small town with limited local opportunities including a textile plant, a guitar company, and cement manufacturing.

4) Andover, Massachusetts: Andover is a suburb of Boston and features good schools and scenery. It is 20 miles north of Boston. It has an excellent college prep school and a rich history that dates back to the 17th century.

3) Ridgewood, New Jersey: Ridgewood is 20 miles northwest of Manhattan. You can commute by rail. There are good schools here and the downtown is charming. You might even be able to get away with not owning a car here.

2) Southington, Connecticut: This town is 20 miles southwest of Hartford, the state capital. You should be able to commute easily using the highways. The median income is over $110,000.

1) Gahanna, Ohio: This city is a suburb of Columbus, the state capital. Columbus international airport is nearby. There are always a lot of jobs at large airports. In addition, there are a variety of jobs in Columbus including manufacturing.

So there you have it: the top cities for 2023. As you can see, affordability is a big component of what is driving housing decisions. This is the first time that Realtor.com has only two regions represented, those were the Northeast and the Midwest. Almost all of the ten feature more living space. You are seeing inventories struggling to keep up with the quick pace of sales. Buyers are generally well qualified because the housing market is competitive.

Works Cited:

https://www.realtor.com/research/hottest-zip-codes-2023/?utm_source=Iterable&utm_medium=email&utm_campaign=campaign_7707852

Tags:

best cities, top 10, best cities to live in, best cities in america, best cities to move to, us largest cities, us cities, best cities to live in america, cities, american cities, top ten lists, top 10 cities to live in usa, top 10 cities us, most populated cities in the us, top us cities by population, top 10 cities in the us, top usa cities, top 10 cities to live in us, worst cities in america, biggest cities, top 10 usa cities, real estate, real estate investing, real estate agent, real estate market, investing in real estate, how to invest in real estate, real estate crash, real estate investment, texas real estate, real estate bubble, houston real estate, real estate investor, invest in real estate, how to make money in real estate, real estate 101, real estate investing for beginners, real estate business, real estate coaching, real estate training, new real estate agent

178

views

2023 Cruise Industry Update

2023 Cruise Industry Update

Cruise tourism is expected to exceed pre-pandemic passenger volumes by 6%. This contrasts with the rate of overall international tourism which is only 80 – 95% of 2019. In fact, cruises continue to be one of the fasters growing sectors of tourism.

The world’s largest cruise port operator, Global Ports Holdings, reported nearly twice as many passengers for the three months from April through June, leading to a quarterly revenue increase of 60%.

There appears to be clear enthusiasm for cruising by the public. Current global cruise capacity is ~644,000 and is expected to increase 19% to 746,000 in 2028. Some estimates put the number of cruise passengers at 40 million per year by the end of 2027.

Younger generations are driving demand for tourism.

88% of Millennials and 86% of Gen-X travelers who have cruised before say they plan to cruise again.

77% of Millennials and 73% of Gen-X express interest in cruising.

Younger cruise travelers are more likely to turn to travel advisors to book their cruises than older generations.

Younger cruise travelers are also traveling with older generations. Multi-generational cruise travel looks set to increase.

Cruise lines are offering shorter and longer cruise itineraries to attract first time guests. Despite adding both short and long voyages, there is more demand for longer cruises, especially among repeat cruise guests.

The Big Three Cruise Lines

The share prices of the big three cruise lines are up big this year. Carnival is up over 90%, Royal Caribbean has doubled, and Norwegian Cruise Line is up almost 40%.

Royal Caribbean experienced record-breaking demand for its new flagship Icon of the Seas which is slated to set sail later this year. The ship can host more than 5,600 guests across 6 waterslides, 7 pools, 19 floors, and over 40 bars and restaurants.

The decade from 2010 to 2019 led to Carnival Corporation making over $24 billion in operating profits, $3.3 billion of which in 2019 alone. The cruise line almost went bankrupt during the first three years of Covid-19.

Despite a surge in revenue, Carnival Corporation reported an operating loss of $4.4 billion in 2022. The company faces significant operating expenses. For example, Fuel alone was $2.2 billion in 2022.

Trends

Solo cruises travel is on the rise as more single-cabin capacity is being added to new ships. Existing ships are being retrofitted for solo travelers.

There is a focus on being environmentally friendly. LNG is being emphasized as a transitional fueld as new fuel and propulsion technology is explored. LNG is the cleanest fueld available at scale, and is becoming more readily available.

The Carribeean remainds the top destination for cruise travelers followed by Europe, Alaska, and the West Coast of North America.

If we look at this visual you see average guest age on the X-axis, and average length of days in the y axis. It appears that cruises in asia are shorter and attract a younger crowd. Australia, New Zealand, and Pacific cruises tend to draw an older crowd for a length of between 7 to 8 days. Scandinavia and Iceland cruises are among the longest with an average length of over 10 days.

The top ports include Miami, Port Canaveral, Cozumel, and Port Everglades.

Luxury Cruise Market

The luxury cruise market is expected to carry over 1 million guests in 2023 versus 600,000 in 2019.

Most cruise ships maintain a ratio of 1 crew member for every 2 to 3 passengers.

The National Geographic Islander II is part of an alliance between Lindblad Expeditions and National Geographic travel. The ship accommodates only 48 passengers and offers a 1:1 guest-to-crew ratio. It is based on the Galapagos Islands.

Works Cited:

https://read.chartr.co/newsletters/2023/9/10/cruising-back

https://www.wsj.com/story/six-lessons-learned-from-a-sold-out-cruise-vacation-212cea68?mod=Searchresults_pos2&page=1

https://www.nationalgeographic.com/expeditions/ships/national-geographic-islander-ii/

https://cruising.org/-/media/clia-media/research/2023/2023-clia-state-of-the-cruise-industry-report_low-res.ashx

Tags:

cruise, cruise tips, cruise advice, cruise news, cruise ship, cruise tips and tricks, first time cruise tips, cruise vacation, cruise travel tips, life well cruised, msc cruises, cruise travel, cruises, cruise ships, msc cruise ship, cruise tips for travellers, cruise tips for first timers, msc cruise, cruise information, cruise vlog, cruise vlogs, first cruise, cruise review, cruise ship tour, cruise trip, luxury cruise, cruise ship review, largest cruise ship, cruise passion, top 10 cruise trips, cruise trip on a budget, cruise trip cost breakdown, cruise ship food

299

views

The Cable TV Endgame is Here: Disney vs. Charter Communications

The Cable TV Endgame is Here: Disney vs. Charter Communications

The ~$200 billion TV industry is starting to crumble as the foundation laid by a decades long alliance of programmers and distributors begins to give way.

Over the past decade, ~42 million US households have abandoned traditional pay TV plans. Most of these households gave up on live television entirely. The cable-TV industry thrived for decades based on the model of charging users for more channels than they could possibly watch. The cable providers then paid out a portion of the fees to channels they carried. Entertainment giants steadily began demanding larger fees for their channels, which drove up the price of cable further, and resulted in more consumers cutting the cord. Contrast this with the relatively low price of a service like Netflix. At this point, I would argue the main selling point of the traditional cable TV package is live sports, but now both ESPN+ and Peacock have exclusive NFL games on their platforms this season.

Disney’s fight with the nation’s number 2 pay TV provider, Charter Communications could represent the endgame for cable TV as we know it. Charter has almost as many pay TV subscribers as the number 1 pay TV provider, Comcast.

Charter’s cable service is called “Spectrum. This latest feud has left 15 million customers of Charter’s Spectrum cable service without access to Disney’s ESPN and other channels. Charter has suggested it may exit the pay-tv business entirely. This is a threat they may very well make good one and I am going to tell you why shortly.

There is an existential threat for Charter that its customers will walk away from it during the standoff with Disney and not return. However, Disney is also losing access to millions of households too. Disney makes a significant amount of revenue from cable, especially for ESPN which is about 75% of what it is charging for given how expensive the rights for sports are. Cable is the cash cow for the television industry, and specifically entertainment programmers like Disney. They use money from cable to produce new shows that they can put on the streaming services. Cable is effectively subsidizing streaming. Consumers are rapidly cutting the cord and abandoning cable TV at an accelerating pace. This, in part, is enabled by companies like Disney, Warner Bros. Discovery, and Paramount Global which have made high value cable content available through their streaming services.

These companies are trying to strike a balance that is all but impossible: allowing cable tv to somehow wobble along so they can turn around and plow those profits into streaming services which are currently losing billions of dollars a year collectively. Said another way, they are trying to keep milking the legacy cable-TV as long as possible to prompt up unprofitable streaming business until it can become profitable. The balancing act is to not kill the cable TV model entirely because that money is needed to keep supporting streaming until it can stand on its own two legs. Pay TV companies are effectively subsidizing streaming, which is cannibalizing cable TV. The chief content officer at DirecTV describes it as “Taking our money and weaponizing it against us is a problem.”

Entertainment companies claim they are trying to find ways to include pay TV partners in the shift to streaming, but this is just lip service in my opinion. The relationship between pay cable TV providers and entertainment programmers has become more adversarial, as they two camps have increasingly contrasting goals.

Charter has an conflicting business model. They do not make very much money from cable TV.

Many small cable providers have stopped offering TV bundles to their subscribers and are referring them to internet-TV providers such as Google’s YouTube TV. The broadband internet business is more lucrative and you are increasingly seeing companies pivot towards it. This is why Charter has the strong hand in regards to Disney. There is a 45% overlap between Charter’s internet broadband service area with that of a competitor offering similar broadband services.

Another interesting component of the negotiation is that Charter is demanding that Disney’s streaming apps, which include Disney+, Hulu, and ESPN+, be made available at no cost to its pay TV customers. However, Disney wants to be paid more for these streaming services. Charter believes they are more than adequately compensating Disney for their services. Disney is seeking to portray Charter as abandoning their customers. Charter is going to argue that Disney wants to increase everyone’s cable bill.

Charter says that 25% of its subscribers regularly engage with Disney content. However, more than 25% of its content costs are derived from Disney. Therefore, although Charter could lose subscribers, it is in a position to shed more expenses than it does revenue.

Disney, and the entertainment industry, already face a crisis with the actor and writers’ strike. However, in this case I would argue that Disney is in a better negotiating position than the unions, but in a weaker position versus Charter Communications. The collapse of cable pay tv would be bad for actors and writers as they get paid better for cable TV rather than streaming content. What may happen is that Disney scores a win against the writers and actors, but has to make concessions to Charter.

Charter is threatening to leave TV altogether. This is no longer the early days of cord cutting. Subscribers are leaving quickly.

Disney’s free cash flow has been greatly diminished as of late. They want to hold on to revenues from cable to staunch the bleeding that is the losses from streaming until it becomes more profitable. The thing is, I’m not sure streaming will ever be as profitable as people think. It hasn’t been thus far, and I’m not sure what would allow losses to pivot towards profits. Streaming services will have to leverage global scale to become more profitable. The piece that I think many analysts are missing is that a lot of young kids are watching YouTube more than they are watching scripted television on streaming services. This miscalculation may mean that streaming is less profitable than many analysts think.

ESPN

In the early days of cord cutting, when there was a loss of subscribers, this would result in a reduction of the carriage fees earning by the entertainment companies, which would then turn around and demand a larger fee per subscriber from pay tv companies. Disney in particular had a strong hand because it had ESPN and that was the main event on television. Sports is perhaps the only thing that is holding strong on television. The audience skews young.

Charter wants the freedom to not offer ESPN. ESPN is the most expensive thing in the cable bundle by far. Disney charges Charter an estimated $12.50 for all Disney bundled channels. ESPN is roughly three-quarters of that. If Charter can eliminate EPSN, that would make the cable bundle significantly cheaper.

Charter argues that being tied to ESPN makes them less competitive. They would prefer to sell skinny bundles which are stripped down bundles. They believe they can slow the decline of TV subscribers this way.

Disney is preparing to launch an ESPN streaming service. ESPN+ has many subscribers but this could because it is bundled with Disney+ and Hulu. ESPN+ doesn’t encompass the same full suite of sports rights that ESPN the cable channel has. The future ESPN streaming service could be as much as $25 or $30 a month. Sports fans are not used to paying the full bill because people that do not watch sports have effectively been subsidizing ESPN on cable. It is interesting that despite sports being so popular, they are effectively subsidized. ESPN is being charged to everyone that pays for cable, not just the people that watch sports. It turns out you have to charge quite a lot for sports. There has been runaway inflation for sports TV right partly because of the traditional cable tv subscriber fee model.

ESPN may partner with sports leagues. They could go to the sports leagues and offer to share the revenue together. This is not an easy thing to make happen.

What matters is where people go for their sports.

$4 billion in free cash flow for Disney in regards to this dispute.

Conclusion:

Disney is going to most likely make out worse. Despite Disney being the much larger company, it has more to lose and could well cave to Charter’s demands. Disney reportedly plans to reinstate its dividend and needs to maintain revenues from cable television.

Other pay tv providers, as well as streaming companies, are holding their breath and watching the action between Disney and Charter.

I don’t think anyone will really be celebrating the outcome.

Works Cited:

https://www.wsj.com/business/media/disney-spectrum-espn-charter-dispute-9147744b?mod=hp_lead_pos7

Tags:

spectrum, charter spectrum, espn charter spectrum, charter, espn spectrum, spectrum cable, charter spectrum new york, charter communications, charter spectrum commercial, disney spectrum dispute, disney espn spectrum, disney spectrum blackout, charter spectrum internet self install, spectrum jobs, espn charter dispute, spectrum internet, spectrum tv, espn charter, spectrum internship, hulu spectrum, spectrum remix, spectrum cable channels, disney spectrumdisney, disney news, disney parks, woke disney, charter disney dispute, failing disney, disney spectrum, disney blackout, disney backlash, walt disney, disney+, disney stock, disney world, disney characters, disney channel, charter espn dispute, charter espn channel, charter cable, can disney stock recover, disney shadows, espn, disney, disney espn, geeks and gamers, espn blackout, disney espn hulu, spectrum espn disney, disney cable espn, can i watch espn on disney plus, disney espn layoffs, can you watch espn on disney plus, disney espn layoffs 2023, how to watch espn on disney plus

97

views

The Traditional TV model in 60 seconds

The Traditional TV model in 60 seconds

You have the companies that make the shows and stick the shows on the channels. These are called programmers and Disney is an example of a programmer. Programmers make money in two ways. One way is to get the cable companies, called Multi-channel video programming distributor, to pay them to put their channels in the cable bundles. This is called carriage. They are carrying the channels. The second way is to sell advertising.

Cable companies make money by charging subscriptions to their customers for the cable bundles. They also get a small amount of the advertising slots. The traditional cable business is a gold time. Customer pay for both the things they want and don’t want. In addition, customers then have to sit through advertising.

While watching cable, you may have noticed a mix of both national advertisements and local advertisements. This mix of different ads is because some ad spots are controlled by the network while others are controlled by the local cable company.

Cable is the cash cow for the television industry. They use money from cable to produce new shows that they can put on the streaming services. Cable is effectively subsidizing streaming.

Tags:

disney, charter, disney news, charter spectrum, disney spectrum dispute, disney spectrum blackout, disney parks, woke disney, charter disney dispute, failing disney, disney spectrum, disney blackout, disney backlash, disney espn spectrum, walt disney, disney+, disney stock, disney world, disney characters, disney channel, charter espn dispute, charter espn channel, espn charter dispute, charter cable, can disney stock recover, disney shadows

37

views

Real Estate Paradox: High interest rates but also high prices

Real Estate Paradox: High interest rates but also high prices

Can you guess the thing that American report they want the most out of life? It is homeownership.

This is lies at the heart of the American dream. However, the American dream has rarely ever been this hard to attain. Prospective homeowners face a triple threat of high prices, costly mortgages, and low housing supply. This had led to a feeling in the country that home ownership is unaffordable and there is little sign of this changing in the future.

Housing is usually some of the most sensitive sectors to interest rates. However, economics has never been so convoluted as today.

After the Federal Reserve went on the offensive against interest rates, mortgage rates soared from 3% to 7% in less than two years. The mortgage payment for the median home doubled from roughly 14% of monthly income in 2020 to nearly 29% in June. This is the highest rate since 1985.

What is perplexing is that the jump in mortgage rates has not led in turn to a decline in house prices. While home prices dipped briefly when interest rates began to rise, they rebounded to record highs shortly thereafter. This rebound seems to be gaining strength. When you annualize second quarter home prices, they rose at a pace of 15%.

The American property market has approximately $2 trillion in sales annually. Some regions are flourishing while others are contracting. The CEO of one of the biggest homebuilders, Toll Brothers, said that “there are still buyers out there. They have very few options.”

While there has been a decrease in demand for homes, this has been offset by a decrease in supply.

The 30 year fixed mortgage is something unheard of in most of the world but it is viewed as a constitutional right in America. This is enabled by Fannie Mae and Freddie Mac, two government backed firms, buying mortgages from lenders and securitizing them. Long term fixed rate mortgages allow American to buy homes. However, these long term rates are now an impediment. People with low mortgage rates effectively have golden handcuffs that prevent them from selling their properties because they would lose their favorable loans. Redfin estimates that 82% of homeowners have mortgage rates below 5%.

You would think that the decline in real estate transactions would hurt the economy, but that does not seem to be the case. American homeowners, refusing to give up their mortgage loans, have resorted to fixing up their current homes. This has been further reinforced by remote work. Remodeling expenditures increased 40% from 2019 to nearly $570bn in 2022.

Many people have decided to build new homes rather than purchase an existing home. This is partly because new construction is more readily available than existing homes. In fact, newly built homes account for nearly one-third of active listings this year.

Homebuilders have been offering incentives to buyers including the ability to “buy down” as much as 1.5% on mortgage rates by paying a one-time fee upfront. This can be the equivalent of knocking 6% off the selling price of a home. This may actually be a smart move for homeowners if interest rates remain elevated. The low interest rate environment that has existed for year is a peculiarity that is not in line with historical interest rates. Interest rates now are more in line with historicals, and this may lend credence to the idea that they will stay elevated for some time. I would advice you not to count on the fact that you will be able to refinance in the next couple years to a rate less than 5% unless there is grave economic turmoil.

Many analysts, including myself, are wondering how long real estate price resilience can continue. Mortgage rates are likely to climb higher as the Federal Reserve increases interest rates. However, the higher interest rates go, the more real estate demand falls. This may encourage lenders to offer riskier deals to capture business. If the real estate market remains strong, it is the Federal Reserve that will be tested. A strong housing market contributes to an overheating economy. This relationship is not straightforward because property values tend to show up in inflation gauges in the form of rent. Rents have decline somewhat, and that is now starting to filter through to inflation measures.

The future is uncertain. There are a record number of apartment building under construction, and this should reduce rents. However, you also have a very unaffordable housing market that is pushing prospective buyers to the rental market instead of purchasing a home. What I can tell you is that as long as interest rates remain so high, Americans will have to defer their dream of homeownership.

Works Cited:

https://www.economist.com/finance-and-economics/2023/08/30/how-can-american-house-prices-still-be-rising

Tags:

real estate, real estate market, real estate crash, housing market, real estate market today, real estate investing, real estate market predictions, housing market 2023, housing market crash, stock market, real estate 101, real estate agent, how to invest in real estate, housing market forecast, real estate bubble, real estate 2023, us housing market, stock market news, investing in real estate, how to make money in real estate, real estate agent tips, real estate agent 2023, real estate investment, real estate code, real estate in 2023, real estate broker, real estate school, real estate canada

170

views

6 reasons you should be maxing your HSA contributions

6 reasons you should be maxing your HSA contributions

1. Triple Tax Advantage: contributions to your HAS are tax-deductible which means they reduce your taxable income. The money in your HAS grows tax-free. Withdrawals for qualified medical expenses are tax-free.

2. Retirement Fund: HSAs can function as retirement savings tools. Money that you do not spend on medical expenses can be invested into the stock market and grow significantly over time. Your HSA funds can take advantage of the magic of compound growth in the market which can lead to substantial savings and investment growth. After you reach the age of 65, you can withdraw the funds for non-medical expenses without penalty, but you will have to pay income tax like how a traditional IRA works.

3. Emergency Fund: Your HSA can act like an emergency fund for unexpected medical expenses. By maximizing your contributions, you can have a substantial financial cushion of medical expenses. Health care costs can be substantial and will most likely only increase in price and frequency as you age. It is prudent to start contributing money towards your HSA now, so the money can grow in the stock market, and provide for future medical expenses in the future.

4. Employer Contributions: If your employer is contributing to your HSA, you should max your contributions to take full advantage of employer contributions. Employer contributions are part of your overall benefits and compensation package. It is effectively free money if you fulfill your end of the bargain: contributing to your HSA.

5. Flexibility: HSAs have a great degree of flexibility in how you can use the funds including deductibles, co-pays, prescriptions, dental care, and even certain things at the store if they are medical related.

6. Portability: Your HSA is portable which means it is not tied to your job or insurance plan. You can keep your HSA funds when you switched jobs or insurance providers.

You should note that HSAs have contribution limits set by the IRS. For 2023, the annual contribution limit for individuals with self-only coverage is $3,750, and for those with family coverage, it's $7,500.

Tags:

health savings account, health savings accounts, health savings account explained, what is a health savings account, health savings accounts explained, health savings account (hsa), health savings account rules, health savings account limits, best health savings account, hsa accounts, fidelity health savings account, how to use health savings account, health savings account investing, health savings account definition, hsa, hsa explained, hsa accounts, hsa contributions, hsa contribution, hsa accounts explained, what is an hsa, hsa investment, hsa investment options, hsa contribution limits, hsa accounts for fire, how to use hsa account, how to open hsa account, hsa benefits, hsa contributions for s corp, hsa bank, hsa contribution limit, making contributions to hsa, hsa contribution penalty, lively hsa, hsa contribution deadline, hsa excess contribution, hsa contribution limit 2024

78

views

The Visa and MasterCard Duopoly

The Visa and MasterCard Duopoly

Did you know that when you pay with your credit card, approximately 2% to 3% of that entire amount goes back to the bank that issued your card? This is called the interchange fee or swipe fee. Some of that money is paid out to cardholders in the form of rewards like cash back or airline miles. Another piece of the interchange fee is paid to payment networks like Visa and Mastercard.

Did you notice that I said “card issuing bank?” Visa and Mastercard to not issue cards directly to the public but Discover and American Express do. The card issuing bank actually issue the Visa and Mastercard credit cards to customers. Visa is larger than Mastercard in terms of transactions, purchase volume, and cards in circulation. It really doesn’t matter much whether you have Visa or Mastercard. What matters is the bank issuing the card. The bank determines interest rates, fees, and rewards. The only time it really does matter whether you have Visa or Mastercard is when you go to a merchant like Costco, that only accepts one and not the other.

The interchange fee helps compensate the card-issuing bank for various costs associated with providing credit card and debit card services such as fraud protection, customer service, and card issuance. Did you know you have more consumer protection with a credit card than a debt card? If you can be responsible with your credit card and pay off the balance, you should be doing all your transactions on your credit card rather than your debit card.

US merchants paid $93 billion in Visa and Mastercard credit card fees last year.

The companies have an operating profit of more than 50%.

The combined operating profit of Visa and Mastercard has grown 40x in less than two decades to more than $31 billion last year.

Most retailers have very slim profit margins. What people do not realize is that businesses expenses, whether they result from shoplifting, or in this case, credit card fees, are in turn based on to the consumer. However, most merchants will charge you the same amount whether you pay with a credit card or cash. Therefore, there is a transfer of money from people that pay with cash to people that pay with credit cards.

Visa and Mastercard have both announced they plan to increase fees paid by retailers.

Works Cited:

https://www.investopedia.com/articles/personal-finance/020215/visa-vs-mastercard-there-difference.asp

https://www.wsj.com/articles/the-credit-card-fees-merchants-hate-banks-love-and-consumers-pay-11592731800?mod=article_inline

https://www.wsj.com/finance/visa-mastercard-prepare-to-raise-credit-card-fees-ed779be1?utm_source=chartr&utm_medium=newsletter&utm_campaign=chartr_20230901

Tags:

interchange fees, interchange, interchange fees explained, visa interchange fees, interchange fee, interchange fees for credit cards, interchange fee (business operation), interchange rates, interchange plus, interchange plus pricing, what are interchange fees, how interchange fees work, interchange fees meaning, high visa interchange fees, mastercard interchange fees, credit card interchange fees, payment card interchange fees, interchange rate, credit cards, best credit cards, credit card, best credit cards 2023, best cash back credit cards, travel credit cards, cash back credit cards, credit cards for beginners, credit, best travel credit cards, credit score, top credit cards, credit cards 101, chase credit cards, best credit card, credit cards explained, best credit cards for beginners, best cash back credit cards 2023, credit card debt, 16 credit cards, credit cards 2023, 2022 credit cards

107

views

3

comments

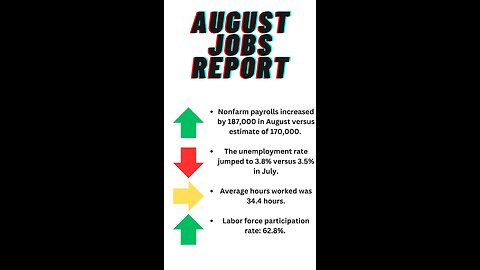

August Jobs Report

August Jobs Report

Nonfarm payrolls increased by 187,000 in August versus estimate of 170,000.

The unemployment rate jumped to 3.8% versus 3.5% in July.

Average hours worked was 34.4 hours.

Labor force participation rate: 62.8%. Highest level since before covid.

Unemployment is rising because of an overall expansion in the labor force not a net decrease in jobs. There are more people looking for jobs for whatever reason. People that were sitting out of the workforce are entering the workforce again. This could be that households need more members earning income to make ends meet. There are more people seeking jobs and fewer people finding them. Unemployment is up because the participation rate increased. There was a net increase in jobs.

My suggestion would be to keep your work performance up and do your best to keep your job. It doesn’t hurt to start applying for some jobs. It will help you gauge the job market in your area and for your profession.

Tags:

august jobs report, jobs report, august jobs report 2022, august jobs report time, jobs, august job report, august, us jobs report, august jobs, august jobs 2022, jobs report today, august employment report, august jobs notification 2022, job report, report, employment report, jobs market, reporting, job, labor department, top stories, economy, us economy, u.s. economy, biden economy, economy explained, economy news, economy live, split economy, world economy, china economy, global economy, indian economy, us economy 2023, economy rescue, economy of china, biden on economy, american economy, us economy crisis, joe biden economy, biden economy live, united states economy, biden economy speech live, economic divide, economic crisis, the economy of united states, economic cool down

122

views

Grayscale Wins in Court! SEC is “arbitrary and capricious”.

Grayscale Wins in Court! SEC is “arbitrary and capricious”.

Grayscale sued the SEC last year after its application for a bitcoin ETF was denied.

The SEC has been ordered to reconsider Grayscale Investments’ application to launch a bitcoin ETF after a federal appeals court ruling on August 29th. Coinbase stock rose 14%. The Grayscale Bitcoin Trust (ticker: GBTC) is up over 18% as of now.

Circuit Judge Neomi Rao wrote on behalf of the court composed of three judges, two of whom were appointed by democrats. “The denial of Grayscale’s proposal was arbitrary and capricious because the Commission failed to explain its different treatment of similar products.” She is referring to the SEC approving bitcoin future ETFs.

This is just another setback for the SEC led by Gary Gensler. The opinion of this channel is that Mr. Gensler is arbitrary and refuses to work with the business sector. This man characterizes everything wrong with government bureaucracy.

Works Cited:

https://www.wsj.com/finance/regulation/grayscale-wins-lawsuit-against-sec-over-bitcoin-etf-1b305cfa?mod=hp_lead_pos4

Tags:

grayscale bitcoin trust, bitcoin, grayscale bitcoin, grayscale, grayscale bitcoin trust discount, grayscale bitcoin etf, bitcoin news, grayscale bitcoin trust stock, bitcoin etf, grayscale bitcoin trust vs etf, bitcoin price, grayscale's bitcoin trust, bitcoin today, bitcoin news today, grayscale investments, gbtc vs bitcoin, grayscale bitcoin investment trust, bitcoin investment trust, bitcoin price today, grayscale btc, buy bitcoin, bitcoin price prediction

47

views

12% of homeowners in the US do not purchase homeowners’ insurance

12% of homeowners in the US do not purchase homeowners’ insurance

Half of those that do not have homeowners' insurance have an annual household income of less than $40,000.

Most mortgage lenders require borrowers to have home insurance, so the people forgoing it often own their homes outright. Those that do have mortgages and don’t purchase insurance will often see their lender buy lender-placed insurance for their property which is generally more expensive.

In some cases, insurers are not renewing policies because of the increased risk of severe damage. Owners may not want state-run insurance policies because they charge a higher premium and offer less coverage.

However, it is the opinion of this channel that a large part of the rise of insurance prices is due to inflation of materials, labor, and just about every construction input for building a house.

While I think most people are fine with not forcing homeowners to purchase insurance, the issue is government assistance is used to bail these people out after a massive natural disaster.

Works Cited:

https://www.wsj.com/personal-finance/americans-are-bailing-on-their-home-insurance-e3395515?mod=hp_lead_pos2

Tags:

homeowners insurance, insurance, home insurance, homeowners insurance 101, homeowners insurance explained, homeowners insurance policies, homeowners insurance coverage, homeowner insurance, homeowners, property insurance, homeowners insurance florida, homeowners insurance 2022, home insurance tips, homeowners insurance guide, homeowners insurance claims, homeowner's insurance, home insurance coverage, understanding homeowners insurance coverage, home insurance florida

40

views

Disney stock is at its lowest price since 2014

Disney stock is at its lowest price since 2014

We are going to explore the headwinds that Disney is facing, and why I think it is a high risk company that is going to continue to face significant challenges going forward.

Disney is a bloated conglomerate that has grown too large and unwieldy to manage.

Disney can be understood as two businesses:

1) Disney Media and Entertainment Distribution (DMED)

2) Disney Parks, Experiences and Products (DPEP)

Disney has significant problems across all its businesses. Linear-TV is in decline. Streaming is a complicated industry, and not as profitable as everyone once thought. The film / studio unit is underperforming. While the parks have had some degree of success, they are not as successful as you would think given that we are past covid.

While most of Disney’s revenues come from media and entertainment, most of the profits come from parks, cruises, and products. If they can address profitability in media, that may be enough to change the direction of the company as a whole. However, I’m not sure there is a scenario where the traditional TV segment becomes significantly more profitable.

Disney is losing money because it is overpaying and underdelivering movies while many movie theaters are going out of business.

Disney hasn’t paid a dividend since 2019.

The Price-to-earnings ratio is still very high. It is about 70 currently versus Netflix at 44,

Movies:

The budgets for films are too high, and the quality is mixed. Everyone from Netflix, DreamWorks, and Sony are running circles around Disney in terms of animation. For example Puss in Boots did much better than Lightyear. The success of the Mario movie shows there is still a market for animation in movie theaters.

ESPN:

ESPN overpaid for sports.

ESPN must still pay the NFL, NBA, and other sports leagues despite cable cutting because of their current contractual agreements. ESPN, and the model as a whole, can not support the leagues’ lofty ambitions and demands any longer.

The deals ESPN made were atrocious and it will take time for them to expire and renegotiate them.

Carriage fees are another significant issue that deserve an entire video in their own right, especially how they pertain to Disney.

Streaming:

Disney spend too much money on content including FOX assets.

There are rumors that Disney will cut its investment into Disney+.

Disney may find some success in licensing its content to other streaming services.

Theme Parks:

Going to a Disney park is a once in a lifetime experience. Once you have done it, and are out a lot of money, and maybe didn’t have the best experience, you are not likely to go back.

There is only so much profit the theme parks can generate.

While I think we all agree that there are is still a lot of attendance at the parks, I would argue the quality has declined. Talking to a coworker that took his family to the Orlando park, I could not believe how much money he spent at Disney. Disney is competing against Universal Orlando which has been adding new attractions, has cheaper ticket prices, and is cheaper.

Television:

There was a time when television and parks were the main profit drivers. Now, television is losing money each quarter, and so is the movie business. Disney+ is also not earning large margins.

I do not really see any prospects for growth. In addition, the overall business model is risky. Just a few bad films can sink the profitability of the media division.

Conclusion:

In conclusion, there are numerous issues with Disney as a company including earnings and financial performance, market trends and competition, especially regarding animation, its debt load, which you could make an argument the company will not have a lot of difficulty servicing, but is significant nonetheless, management issues, valuation and dividend concerns, and quality issues especially with its films. I think Disney could continue to go lower and I just do not see any films that I’m excited for from them or a coherent argument for a turn around.

Tags:

disney stock, stock market, disney stock analysis, stocks, disney stock price, stock market news, is disney stock a buy, dis stock, disney, dis stock analysis, is disney stock a good buy, finance stock, stock, disney stock news, disney stock 2023, disney stock review, disney stock forecast, disney stock earnings, disney plus, buy disney stock, sell disney stock, disney stock drops, disney stock today, disney stock market, disney stock dividend, stocks, stock market, stocks to buy, best stocks to buy now, tech stocks, nvidia stock, stocks to buy now, stocks to watch, tesla stock, best stocks, best stocks to buy, nvda stock, ai stocks, stock market news, stock moe, ai stocks to buy, tsla stock, best ai stocks, stock market crash, finance stock, stock, top stocks, top stocks to buy now, live stock trading, stock market today, stocks today, stock market for beginners, stock picks, nvidia stock analysis

388

views

New York City’s Airbnb Crackdown

New York City’s Airbnb Crackdown

Starting September 5th, New York City officials are going to begin enforcing rules on short term rental stays more aggressively. Hosts of short-term rentals are going to be required to register with the city and meet certain requirements. Hosts must have a Class B status to provide short-term rental stays.

New rules include restricting a host from renting out an entire apartment or home. They also must be present during guests’ short term stay. Airbnb is blocking future dates for bookings and hosts are removing listings.

There are 38,500 Airbnb listings in New York City. Starting September 5th, the city will know which hosts have not registered, and they will likely impose penalties.

Dallas, Philadelphia, and New Orleans have based restrictions on short-term rentals.

Short-term rentals are generally cheaper than hotels.

Less than half of Airbnb’s New York City listings are in Manhattan. In fact, 37% of them are in Brooklyn, an area that has less hotel options in some areas.

At the end of the day, we are talking about private property. Many hosts rely on the extra income to pay their mortgages and continue to live in their homes. Some hosts rent out their homes when they are traveling for work. Many visitors are families who can’t afford to pay for multiple hotel rooms.

Cities blame Airbnb for the lack of affordable housing. However, I would argue that this is the result of restrictive zoning.

Overly restrictive and complex regulation by local government is burdensome and causes abnormalities in the market. Consider how expensive it is to do construction and develop residential projects in the city.

Both Airbnb and hosts are saying that the NYC rules make is near impossible to register for Class B status required to do short-term rentals. The city is facing a staffing shortage. City bureaucracy is infamously slow, but now it is all but grinding to a fault. As of July 25, the city received 1,632 host registrations, yet only 141 have been approved, according to Airbnb.

Even legal Airbnb’s have little chance of being approved by the city in a timely manner. The city is not actually interested in regulating short term rentals. They want to make it impossible for them to operate all together.

I believe this is a misguided effort by the city to increase affordably housing at the expense of visitors. However, I do not see the city address rent controlled apartments. Instead, they are shifting the blame and targeting short-term rentals. This also could be a play by the city to increase hotel occupancy rates.

At the end of the day, you have to follow the money. The city hotels are furious at Airbnb. The city has lost a lot of hotel tax revenue. In San Francisco you are seeing hotels missing mortgage payments. In addition, you have unions associated with hotels and hospitality that are lobbying the city government to target and crack down on Airbnb.

Also, consider how Mayor Eric Adams has signed contracts for hundreds of millions of dollars to house migrants in hotels. This appears to be another way that New York City is trying to appease the hotel industry and drive business for them.